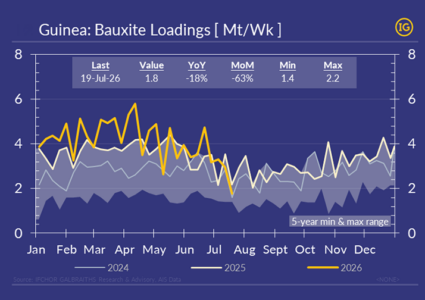

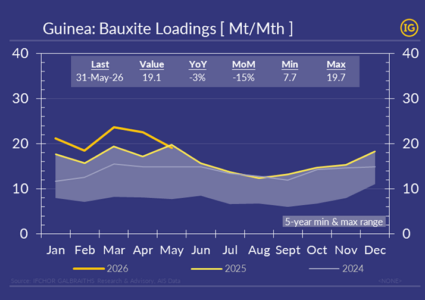

Guinea’s bauxite loadings slumped to 1.3 Mt/wk last week, down -50% WoW and -38% YoY.

Black Sea grain under pressure: what prolonged disruption could mean for freight markets

As disruption persists in the Black Sea, IFCHOR GALBRAITHS Research explores the potential implications for grain exports, freight markets and vessel demand.

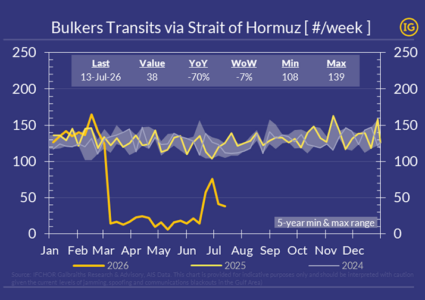

Hormuz: from war risk to transit tolls?

Dry bulk transits through the Strait of Hormuz fell to just 38 vessels last week (-7% WoW, -70% YoY), reflecting renewed geopolitical tensions after the ceasefire collapsed.

Seven freight indicators every dry bulk shipowner should monitor this summer

The analysis is based on IFCHOR GALBRAITHS’ latest Focus On: El Niño & Implications, which examines how evolving weather patterns could influence coal, grains, bauxite, iron ore and key freight chokepoints over the coming year.

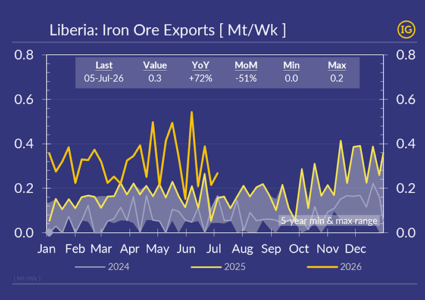

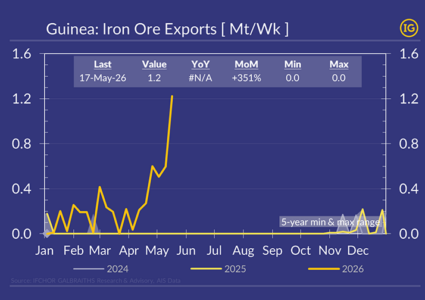

Beyond Guinea: Liberia’s iron ore export boom accelerates

While Guinea’s Simandou project dominates headlines, Liberia is quietly emerging as West Africa’s other iron ore success story.

China now buys 61% of the world’s traded soybeans

IFCHOR GALBRAITHS has launched Agri Markets 360, a new annual research report providing comprehensive analysis of global agricultural trade, export flows, logistics and shipping demand across the world’s major agricultural markets.

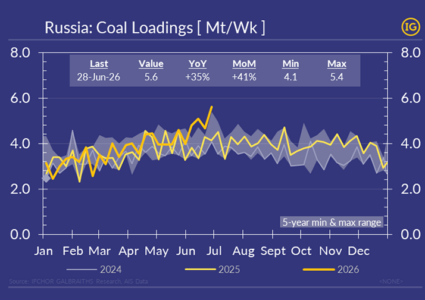

Russian coal loadings hit 5-year high

Russian coal loadings reached 5.6Mt/wk last week, up +41% MoM and +35% YoY to a fresh 5-year high.

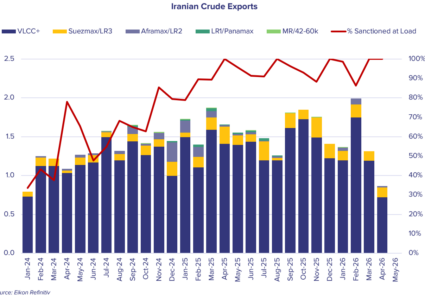

Focus on: Iranian export waivers

A new US sanctions waiver marks a step towards the return of Iranian oil to international markets, signalling potential shifts in global energy markets and tanker demand.

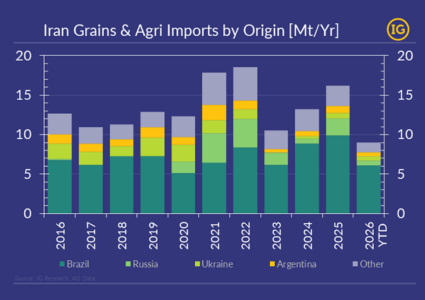

Iran’s grain suppliers unlikely to change despite US talks

Despite speculation that improving US-Iran relations could revive US grain exports, Iran’s central bank governor stated that existing agreements do not require purchases of US agricultural products.

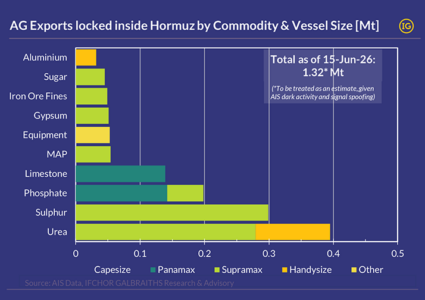

Hormuz reopening may unlock 1Mt of trapped fertilizers, but recovery will be gradual

If the announced framework for a 60-day US-Iran ceasefire is signed on Friday, it could pave the way for a gradual reopening of the Strait of Hormuz, allowing fertilizer cargoes stranded inside the Gulf to resume moving.

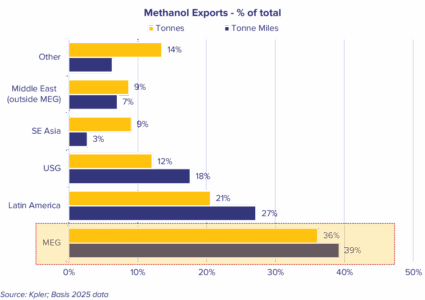

Methanol MEG Export Dislocations

Methanol exports from the Middle Eastern Gulf face significant disruption, driving price increases and supply challenges worldwide.

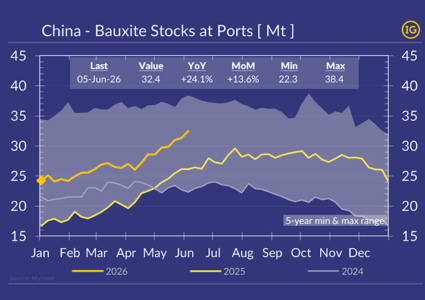

China’s bauxite inventories continue to rise despite firmer prices

China’s bauxite inventories continue to rise despite firmer prices and concerns over Guinean supply.

Laura Gomez: Follow the data and challenge your assumptions

Dry bulk shipping research is not just about data — it is about knowing what matters, what can be trusted, and what the market may be missing.

Guinea bauxite loadings signal tightening global supply

Guinea’s expected bauxite export curbs from Jun’26 are already weighing on shipments.

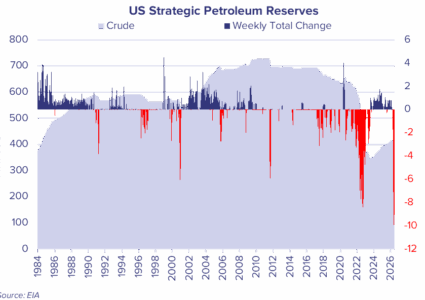

Focus on: US strategic petroleum reserves

Record SPR releases have supported US crude exports and tanker demand. As the programme nears its end, questions over the next phase are growing.

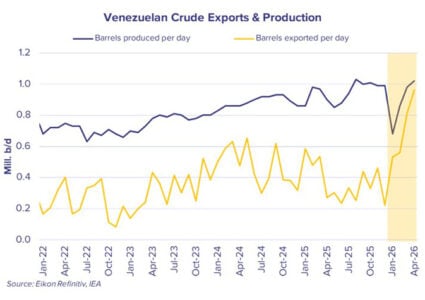

Focus on: Venezuelan oil markets

Venezuelan crude production has exhibited a sharp rebound since the start of 2026, with levels currently sitting at 1.02m b/d, marking the 2nd highest level of production seen since late 2018.

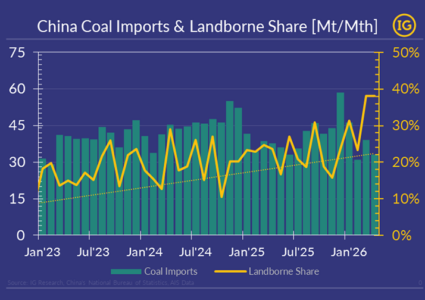

China’s double coal exit: less imports, more by land

China’s coal burn at the six major coastal power groups hit a seasonal high of 0.8Mt/day last week, while Guangdong’s power load reached…

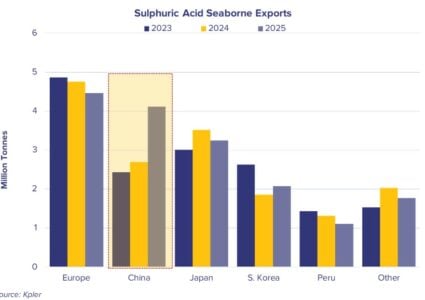

China sulphuric acid export ban

China recently announced a ban on sulphuric acid exports (produced from copper/zinc smelting) from 1 May through to December this year, with other grades except electronic grades heavily restricted.

Why judgement is becoming the scarcest commodity in dry bulk markets

Dry bulk markets have become faster, noisier and more transparent. AIS, pricing and flow data have made parts of the market visible in near real time. Yet visibility is not foresight. Human judgement, context and intuition still determine who stays ahead of the curve.

Guinea: last week saw iron ore shipments above 1.2Mt/Wk

Guinea iron ore exports stepped up sharply last week, doubling WoW from 0.6Mt to 1.2Mt/week.