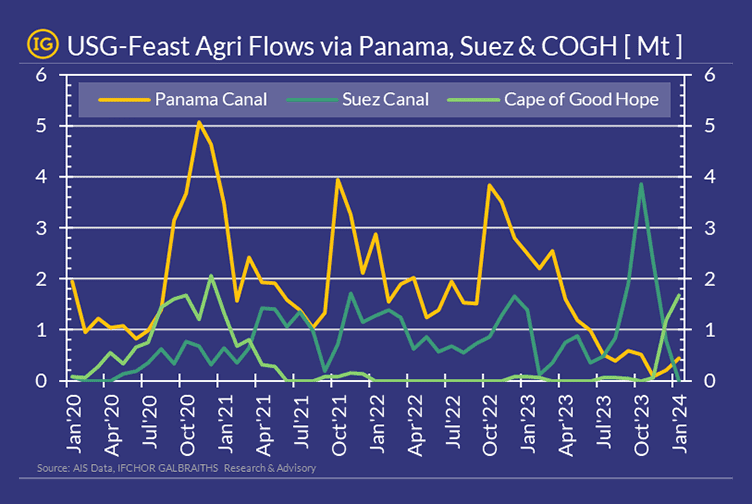

… from the US Gulf (USG) to the Far-East (FE) changed several times in the last months in reaction to several crises! Whilst in normal time, the route via the Canal of Panama is the most used route, the severe drought that resulted in transit restrictions which sent costs up to 4M$ per transit encouraged shippers to explore alternatives after Sep’23. Consequently, the transit through the Suez Canal rose up to 4Mt/Wk in Oct’23 and accounted for ~50% of those exports in 2023. Following the fights in Gaza and the resulting crisis in the Red Sea, the preferred route shifted, again, in favour of the Cape of Good Hope (COGH) from zero before Oct’23 to nearly 2Mt/wk this month.

In spite the longer sailing distances (e.g. +52% for USG-FE via COGH vs Panama), the recorded ton-miles along that route in Jan’24 fell -35% YoY, as shippers had the possibility to switch to alternative suppliers, such as Brazil, or to delay cargo off-take.

If you would like to get more information on this topic and the impact on the freight market, please reach out to us on: [email protected].