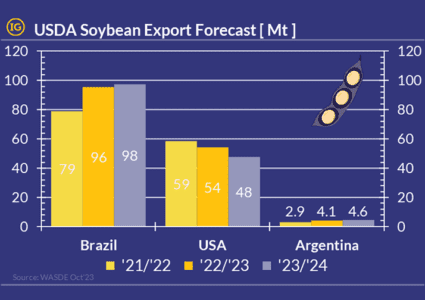

Reading latest USDA forecast, competition for soybean market-share is to remain in favour of Brazil in coming marketing year 23’/’24!

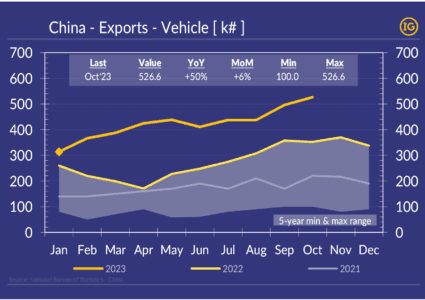

China Exports in October 2023 points at slowing inflation!

Whilst China exports expressed in US dollar terms fell -6.4% YoY and came lower than market expectations, the situation appears more nuanced when considering exports expressed in quantities.

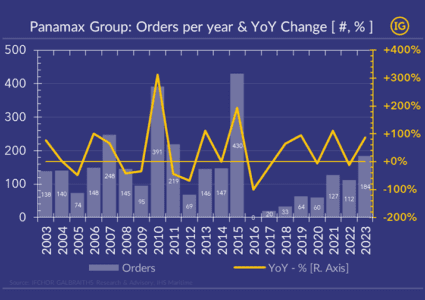

Panamax Group: Orders per year & YoY Change

So far in 2023, Panamax was the bulk carrier segment attracting the most orders with 184 units placed.

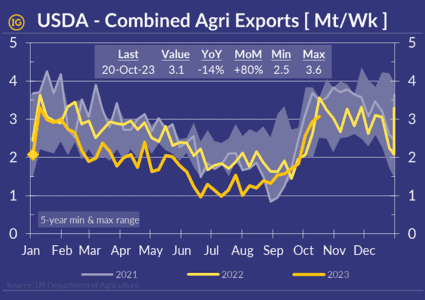

USDA Combined Agri Exports +80% MoM in latest resurgence during harvest period

Combined agri exports out of US has made an astounding recovery in recent weeks, improving +80% MoM to reach levels closer to 2022 albeit -14% YoY lower.

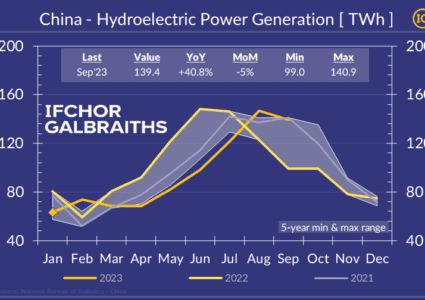

China’s hydropower output up +41% YoY in September was far from covering its overall power demand growth!

Despite hydropower generation in China standing at 5-year seasonal record for 2 months and rising +41% YoY or +40TWh YoY in Sep’23, thermal power generation, primarily from coal, has remained at seasonal record level too and grew +3% YoY during the period.

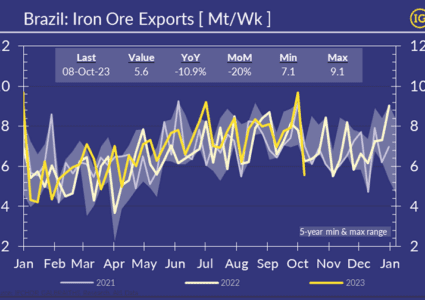

From a 5-year weekly record, Brazil iron ore exports relaxed -42% WoW

After reaching last week a new 5-year record at 9.7Mt/wk, weekly iron ore exports from Brazil relaxed -42% WoW to 5.6Mt/wk, the slowest week on record since Feb’23!

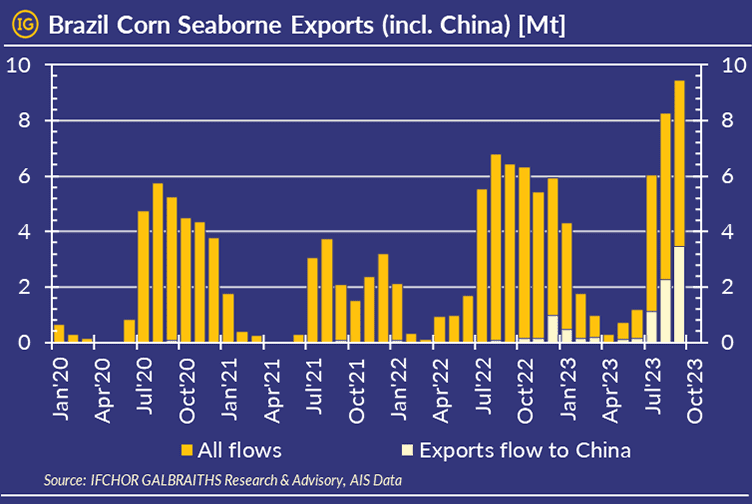

Brazil’s corn exports hit a record, but poor margins could hurt volumes next year

Breaking record for 2 months, Brazil’s corn exports in Sep’23 rose +47% YoY to 9.5Mt, with China consolidating its position of #1 buyer of Brazilian corn (~24% in 2023).

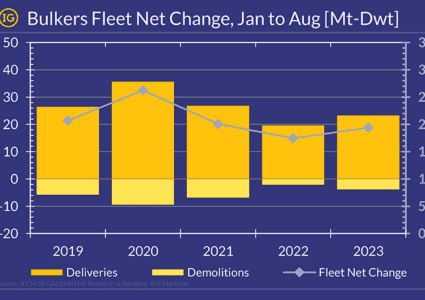

Bottoming in 2022, the growth pace of the Bulk Carrier Fleet accelerates in 2023 (Jan-Aug)

Through Jan-Aug’23, +19.4 Mt-Dwt were added to the Bulk Carrier fleet, equivalent to a +11% or +2Mt-Dwt YoY increase.

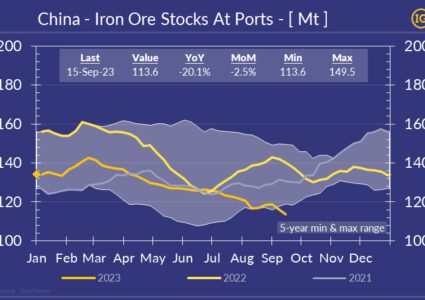

Iron Ore Destocking in Chinese Ports: Impact on Prices and Capesize Rates

Challenging seasonality, iron ore destocking at Chinese ports keeps going and inventories have reached distressed levels supporting iron ore prices & Capesize rates!

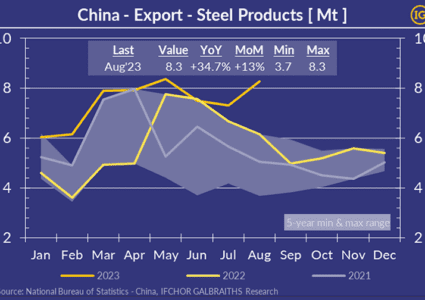

When steel is no longer needed at home, China gets it exported!

Contrasting with previous years, when steel exports were seasonally tracking domestic production and trending lower in the second half of the year, steel exports in Aug’23 unseasonably bounced +13% MoM or +35% YoY to record 8.3Mt/mth.

Potential for Brazil to China tonne-mile gains

Petrobras’ Chief Executive Jean Paul Prates caused something of a stir with recent comments made regarding the planned opening of a Chinese subsidiary.

The top-3 routes for Capesize vessels

Iron ore accounts for more than 60% of Capesize ton-miles, so it is no surprise that two iron ore routes are among the top three ton-mile contributors to the segment.

Brazil corn export season to boost Panamax Fleet Usage

The Summer corn harvest in Brazil is progressing at a rate of +9% WoW, reaching 20% of completion.

Brazil key player behind corn exports tripling over the past 20 years

Over the last 20 years, corn exports increased +174% from 74Mt in 2002 to 204Mt in 2022. This was mostly achieved through Brazil & Ukraine expanding their market share from 4% & 1% in 2002 to 21% & 12% in 2022. Simultaneously, the contribution of the USA was diluted from 61% down to 25%.

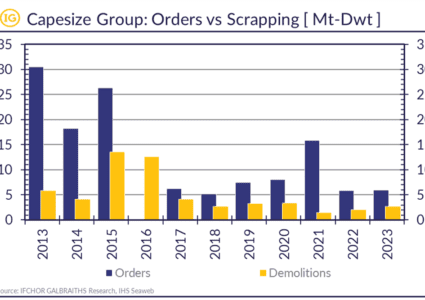

Declining Capesize rates have led owners to renew with demolition after a pause in 2022!

Demolition pace of older Capesize Vessels (130k MT dwt to 200k Mt dwt) is rising & has already exceeded the total volume of 2022! With Capes 5TC spot index trending down lately and the negative macro environment, demolition volumes are set to grow further in the upcoming months!

IG Dry Research Advisors presenting at GrainCom 2023 in Geneva

IG Dry Research Advisors presenting our view on Handy to Panamax Freight Market Outlook at GrainCom 2023 in Geneva