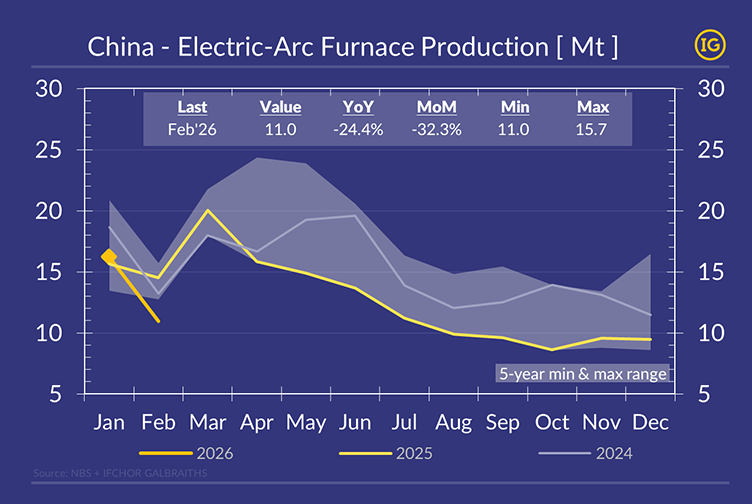

Year-to-date, EAF production reached 27.2Mt in Jan–Feb’26 (-9.9% YoY), lagging Blast Furnace output at 138Mt (-2.2% YoY) and crude steel at 160Mt (-3.6% YoY).

The sharp February drop is partly technical. Lunar New Year shifted to Feb’26 (vs Jan’25), distorting YoY comparisons. But the divergence is real. EAF remains more margin-sensitive and quicker to cut. At the same time, rising iron ore inventories and imports signal weak steel consumption. Without a demand recovery, EAF utilisation is likely to stay under pressure.

For further insights, contact [email protected].