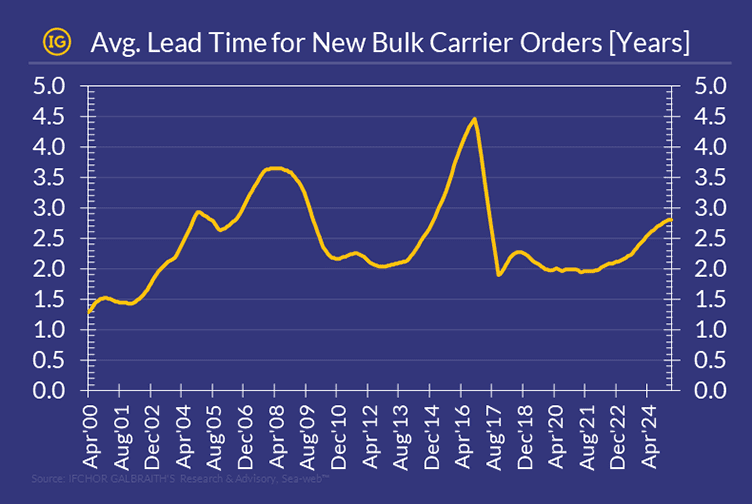

The rise is driven primarily by constrained shipyard capacity and a surge in container ship orders. These higher-margin vessels are being prioritised by shipbuilders, further limiting slots for dry bulk carriers.

This sharp extension in delivery timelines – coupled with macroeconomic uncertainty, persistently elevated newbuilding prices, a peak in the orderbook in 2024, and ongoing uncertainty over future fuel technologies – is deterring dry bulk owners from committing to fresh orders. As a result, bulk carrier contracting in 2025 year-to-date has fallen to its lowest level in 7 years.

For further insights, contact: [email protected].