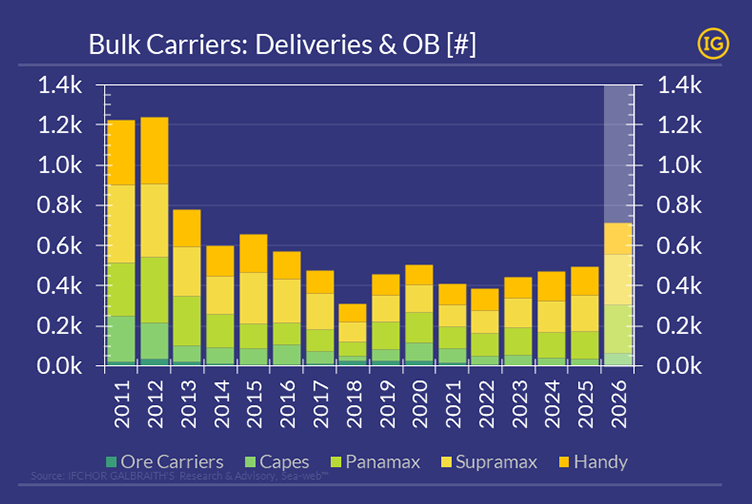

Supply growth is concentrated in the mid-size segments, with Kamsarmax and Ultramax accounting for most incoming capacity. This rapid build in the most commercially flexible ship sizes risks outpacing growth in coal, grains and minor bulks trades, which could temporarily weaken fleet utilisation.

In parallel, the ore carriers (VLOC) segment re-enters the delivery cycle from mid-26 after a pause of nearly 3 years, with owners positioning for expanding long-haul mineral trades between West Africa and Asia.

For further insights, contact [email protected].