The tanker market has had a lot of things to focus on in recent months and weeks; Hurricanes in the US Gulf, escalating conflict in the Middle East, OPEC+ policy adjustment, crude price volatility and Chinese demand levels to name a handful. In the face of some of these many competing forces, the West African tanker market could get slightly overlooked, but there is plenty to discuss and plenty to absorb as we look at future developments and ongoing changes as a result of projects in the region.

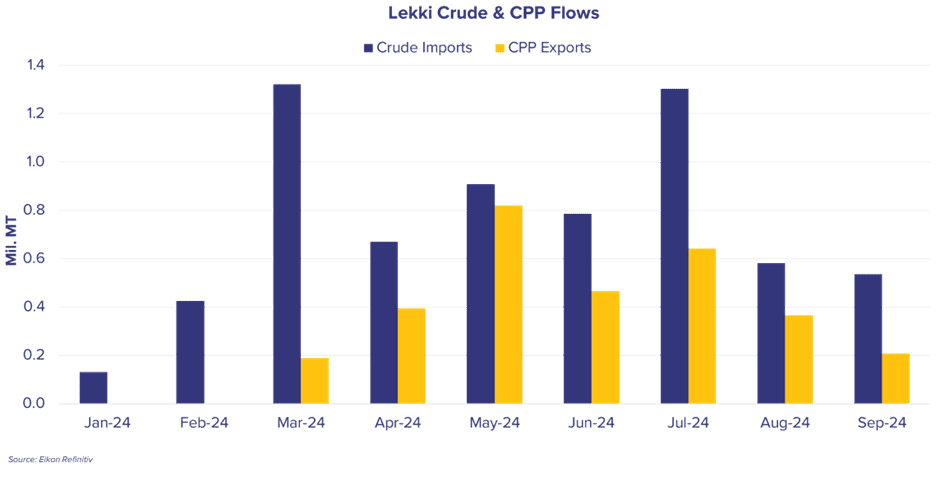

The majority of the recent focus is clearly on Nigeria and the Dangote Refinery project. Much has been written about the use of, or lack of, domestic crude and CPP exports heading into international markets rather than to domestic buyers. On the crude segment, after importing a number of VLCC cargoes from the US at the beginning of the refinery’s operation, these flows have decreased, with the last non-Nigerian cargo being lifted on a VLCC from the Caribs back in mid-August. Equally with CPP exports, the volumes have been notably declining in recent months and weeks from Dangote. In May, 819,000mt of CPP were lifted from the port of Lekki. Throughout August this had dropped to 365,000mt, and further declines have been seen during September, where only 207,000mt has been exported. There clearly remains a significant amount of uncertainty with respects to the feedstock and petroleum production of this project, and it remains a point of significant interest to keep an eye on going forward.

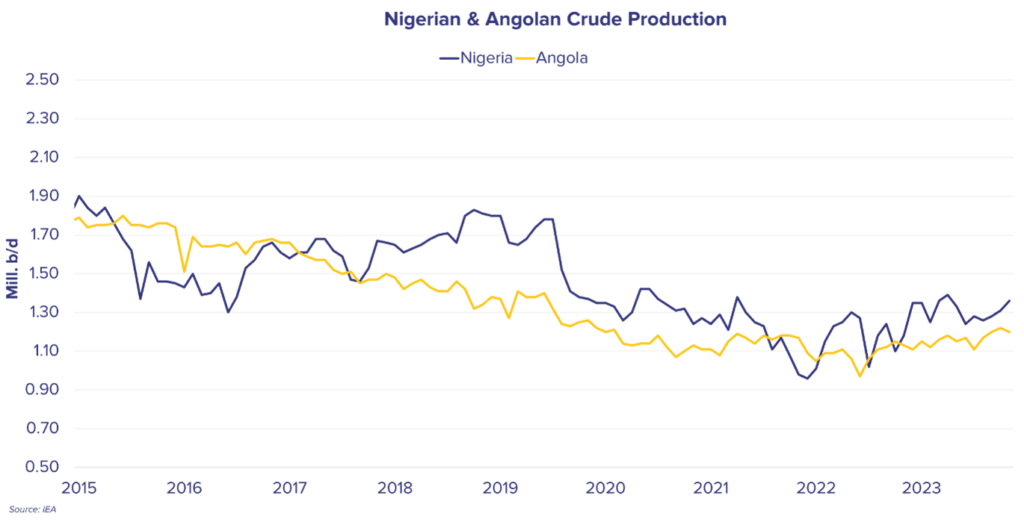

Away from Nigeria, at the beginning of this year Angola stepped away from OPEC, in protest at what the nation viewed as too stringent controls on production hamstringing the nations investment plans for its crude industry, as it looked to stem the long-term declining production levels that had been seen for the best part of a decade. Across 2023, Angola pumped an average of 1.1m b/d, whilst at the time of writing the latest August IEA data pins Angolan crude production at 1.2m b/d. Hardly a dramatic growth, but going forward continued incentives to incrementally increase production from existing developments offer some small upside to crude tankers in the region, with much of this benefit heading towards VLCCs which account for roughly 2/3rds of crude exports.

Other West African nations are looking to play an increasing role in the regional and global crude/CPP markets. Senegal being a prime recent example of this, as production from the Sangomar project began in June of this year. Again, a limited volume to begin with, with Phase 1 of the project producing in the region of 100,000 b/d, however the production has offered another source of West African cargoes for the VLCC markets (which has seen a handful of cargoes heading to Asia) and for Suezmaxes (which has seen a handful of cargoes heading into Europe). In a shifting regional market, these new barrels offer a small bright spot to tankers.

Across 2024 the Ghanaian refinery space has been especially active. January of this year saw the start-up of the Sentuo Oil Refinery, a project with a 100,000 b/d nameplate capacity, although it currently appears beset by delays and limited refinery throughput. In the face of this, the President of Ghana recently ‘broke-ground’ on the construction of a new 300,000 b/d refinery project, with an outlined plan to be in a position to supply the region’s demand for refined products by 2036. However, given the ongoing issues with current Ghanaian refineries, and the known delays that have plagued other major projects in the region, these lofty ambitions may remain ambitions for the foreseeable future.

The West African oil market remain a point of real interest going forward, as the fate of existing projects, and the grand plans going forward, have at least the potential, to reshape tanker demand in the region.