Usually around the beginning of each year, as the market emerges from a Christmas dinner induced sleep, we would be looking at writing a short monthly feature outlining the full picture that 2025 provided from a vessel supply perspective. President Trump clearly has other ideas….

As has so often been the case during his 2nd term (which we feel obliged to remind is still just less than a year old), the tanker market finds itself reacting to significant geopolitical changes. Venezuela has been a regular topic for the Trump administration throughout the past year, although the dramatic ‘extraction’ of President Maduro marks a significant escalation. Setting aside the significant, and ongoing politics of the situation, there is plenty to unwrap for the tanker market alone.

Prior to the military intervention, the US had placed a blockade on crude exports, enforced seemingly through a series of vessel seizures, with the two most recent being the ‘M Sophia’ and the ‘Marinera’. With the US administration now ‘running’ Venezuela, they have publicly signaled their plans for the Venezuelan energy markets. There is an initial tranche of a reported 30-50m barrels of crude that is being marketed by the US government, with sales of Venezuelan crude to continue in this manner ‘indefinitely’ and the proceeds to sit under the control of the US administration. Part of this process will involve the ‘selective rollback of sanctions’, although the scope of these changes is unclear at the time of writing.

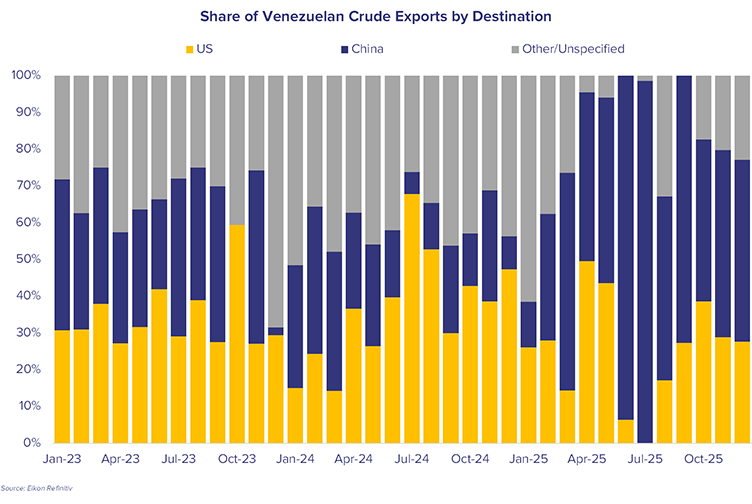

Broadly speaking Venezuelan crude production is significantly down on historical levels, with the latest November 2025 figures having dropped to only 860,000b/d. Prior to recent events, Venezuelan crude has been heading to China and to the US, under the Chevron license agreement which was in place despite the sanctions regime.

If Venezuelan crudes head exclusively to the US, this will leave China with a shortfall in heavy, sour grades. Whilst Chinese refiners will likely be unable to match the discounts offered by Venezuelan grades, there remains some alternatives in the market. Canadian grades could represent an attractive option, with China already taking a significant share of barrels from the expanded Westridge Terminal (China imported an average of 224,000b/d across 2025, with a peak of 359,000b/d seen during the latest full month of November data). Aside from alternate grades, the lack of a discounted feedstock could prompt utilisation reductions Chinese independent refineries.

Notable for the tanker market will be the reduced employment opportunities for the dark fleet. Venezuelan barrels into the US will obviously continue to be taken on market tonnage, a voyage typically employing Aframax sized vessels. A significant share of recent Venezuelan exports heading to China has been on sanctioned tonnage, with even those unsanctioned tonnage used being vessels of a significant age (>15yrs). Replacement barrels into China, either from Canada or other market based heavy grades, will be taken on market tonnage and offer some upside to the tanker market. The sanctioned/older vessels used for Venezuelan business will likely see significantly reduced employment opportunities, with limited options to shift to other sanctioned markets (Russia/Iran). As a result, there could be some increased likelihood of these vessels being removed from the fleet.

In amongst the discussions surrounding Venezuela’s crude exports it is also important to also look at the potential adjustments that could be made with respects to the import of CPP, especially relevant for naphtha imports, which is used as a diluent in order to facilitate the export of the very heavy crude. The US has historically been the source of these volumes, which amounted to around 1m mt through the 1st half of 2025, lifted mostly by LR1s. Russia stepped in as the main supplier throughout the second half of last year, unsurprisingly using predominantly sanctioned tonnage for these flows. The US Department of Energy has already stated that US diluent will flow into Venezuela, likely reopening the trade, which can help offer some additional business to the LR1 segment.

Whilst it feels a little premature to look beyond the next few weeks, the latest statements from the US Department of Energy show a direction of travel for Venezuela that involves the import of ‘select oil field equipment, parts, and services to immediately offset decades of production decline and drive near-term growth’. The tanker market would clearly benefit from any recovery in Venezuelan production, although given the lack of investment and maintenance, any notable recovery is likely to take years of work.