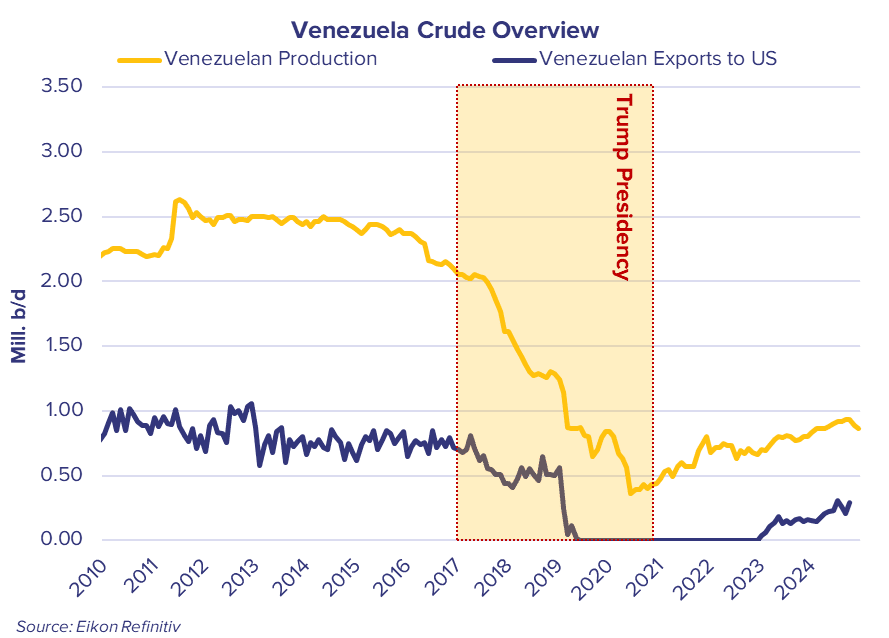

Trump’s first term was characterized with some exceedingly hawkish approaches towards Venezuela, with tight sanctions on Venezuelan oil markets.

Production collapsed, as the market for Venezuelan barrels shrank dramatically. The endgame for the Trump administration was zero Venezuelan crude heading into the US, leaving a much smaller pool of buyers.

The Biden administration lifted some restrictions on Venezuelan imports into the US, although policies remained in flux throughout his term. Chevron currently hold a waiver for imports into the US, thanks to the company’s presence in Venezuela via joint ventures.

Any decision by Trump to revoke Chevron’s licenses will apply significant pressure to Venezuelan exports. This will particularly hold true if the US also chooses to also sanction vessels/entities that continue to lift Venezuelan barrels, and particularly if key buyers in Shandong/India choose to maintain their policy of avoiding OFAC sanctioned entities.

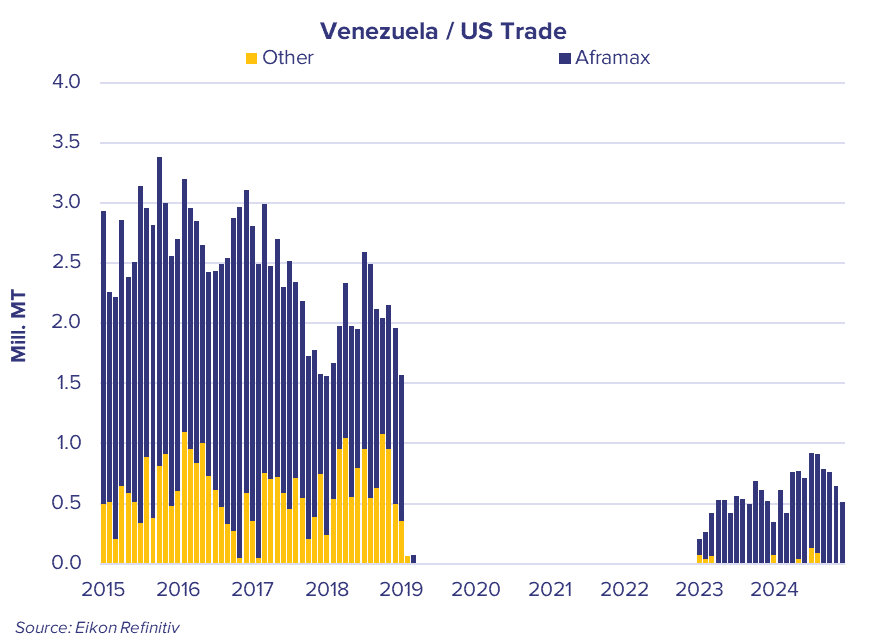

A full embargo on Venezuelan flows into the US, will deprive mostly USG refineries of around 200-300,000 b/d of heavy sour feedstock. The immediate impact would be a drying up of roughly 8-10 Aframax cargoes per month ex-Venezuela into the USG.

Obvious candidates for replacement barrels are regional producers of similar quality crudes; especially South American producers. Mexico may be limited in ability to provide extra barrels, given start up of Dos Bocas and a recent downward trend in barrels heading to the US. Barrels from further afield in the MEG, as OPEC bring back capacity, can offer some further replacements and support tonne-miles.

The overarching question to these replacement barrels, is whether any policy on Venezuelan is completed at the same time as the much-threatened trade tariffs on nearby key crude suppliers, Mexico and Canada especially. If the targeting of local trade partners includes energy, this could force any replacements coming from even further afield. For more information on this topic and others, please do reach out to us at [email protected].