After a landslide win at the presidential elections on the 2nd June for the ruling party’s candidate Claudia Sheinbaum, Mexico will be looking toward the first female President leading the country. Ms Sheinbaum reportedly has plans to overhaul the fuels produced by local refineries in order to boost motor fuel output, according to Reuters.

Focussing on the Olmeca Refinery in Dos Bocas, it is one of the larger refinery projects currently underway in the Atlantic basin, with a nameplate capacity of 340,000 b/d. With a stated aim to reduce Mexico’s reliance on imported petroleum products, construction of the project began in 2019, and whilst announcements about completion and start-up have been made, at the time of writing no crude has yet been processed.

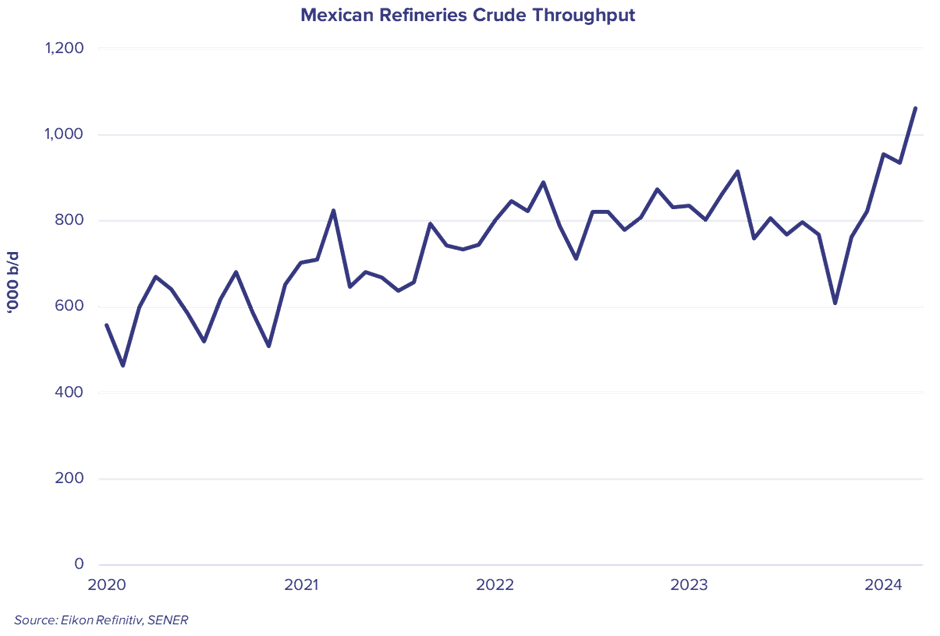

The refinery will come into a refining market in Mexico, which currently has 6 operational refineries with total nameplate capacity of 1.805m b/d. The industry has historically suffered from poor utilization, with even recent improvements in crude throughput only pushing utilisation to circa 59%.

This indicates a scenario where the newly built refinery also operates well below nameplate capacity, helping to limit the potential impact on existing tanker flows.

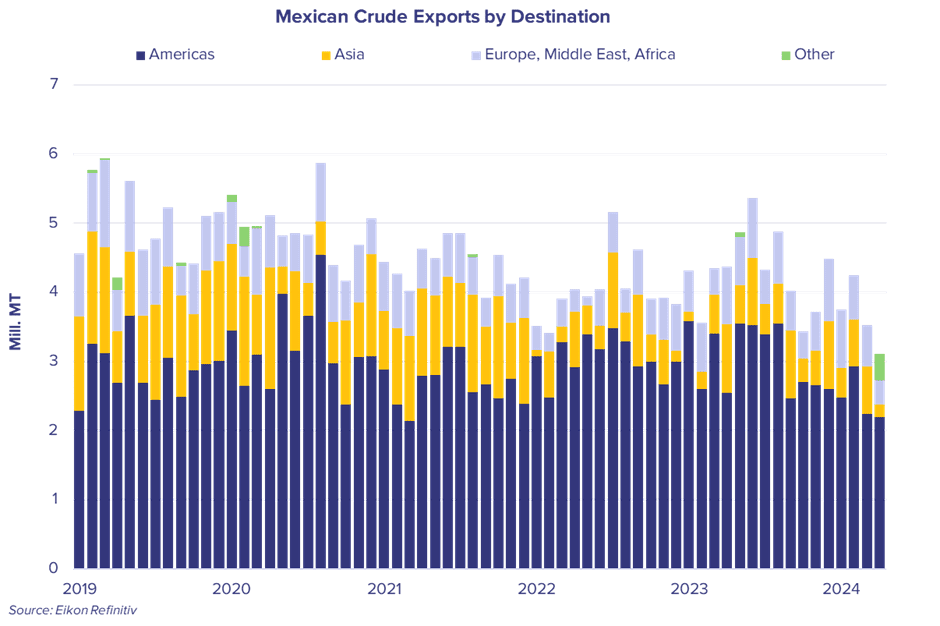

In the current market, Mexican crude is predominantly exported to local markets, mostly the United States. Mexican crude, tends towards the heavy/sour, favoured by the Gulf Coast refiners and increasingly a quality in reduced supply, with many OPEC cuts falling onto this type of crude. Aframaxes are the size to see most significant impact if Mexico sends fewer barrels into the international markets. However, this being said, given the potential twin pressures on US refiners from reduced Mexican exports and the increasing exposure of Canadian crudes to the international markets via the TMX Pipeline, there is the potential that US refiners are forced to look at longer haul barrels to satisfy demand, helping to generate some tonne-mile gains.

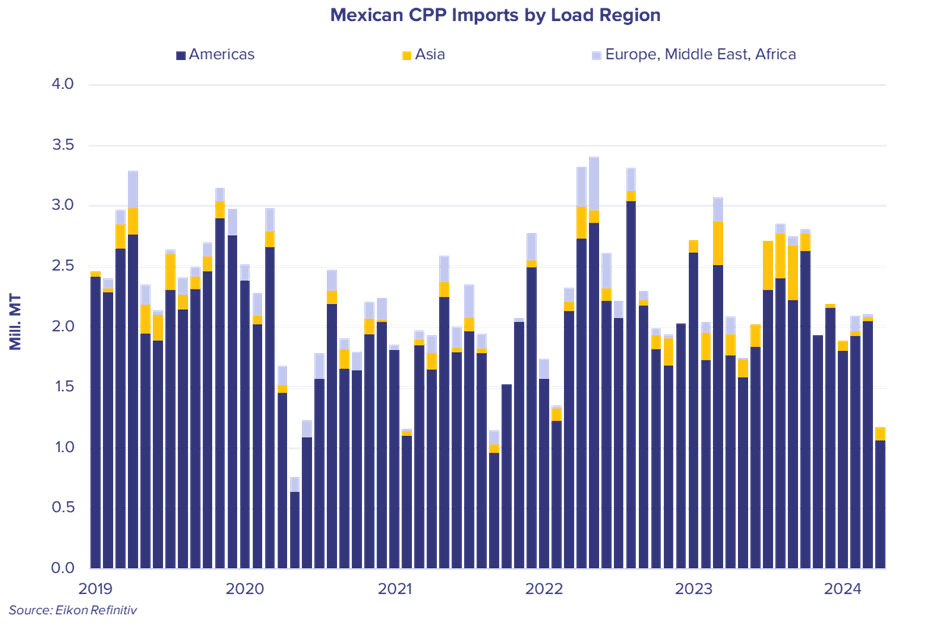

Mexico is traditionally a significant net importer of refined petroleum products, mostly gasoline and diesel. These volumes are coming almost exclusively into Mexico on MR tankers, which stands to be the size most impacted regionally if Mexico begins to satisfy a share of domestic demand with the new refinery capacity.

In 2023 around 89% of these CPP imports came from the United States, pointing towards refiners in the region needing to find an alternative home for these exported products.

Given the geographical proximity of the US and Mexico, any alternative destination is likely to result in an overall boost to tonne-miles.