In amongst the noise of trade policy, sanctions and geopolitical maneuvering it is easy to lose focus on some of the underlying fundamentals of our markets. In the day after “Liberation Day” (“Retaliation Day”?), and with oil, gas and energy products excluded from these latest announced tariffs, we feel it is worth taking a step back to review in more detail the tanker supply picture. We are, after all, in the shipping industry, and the supply of vessels themselves is a fundamental half of the demand/supply picture of our markets.

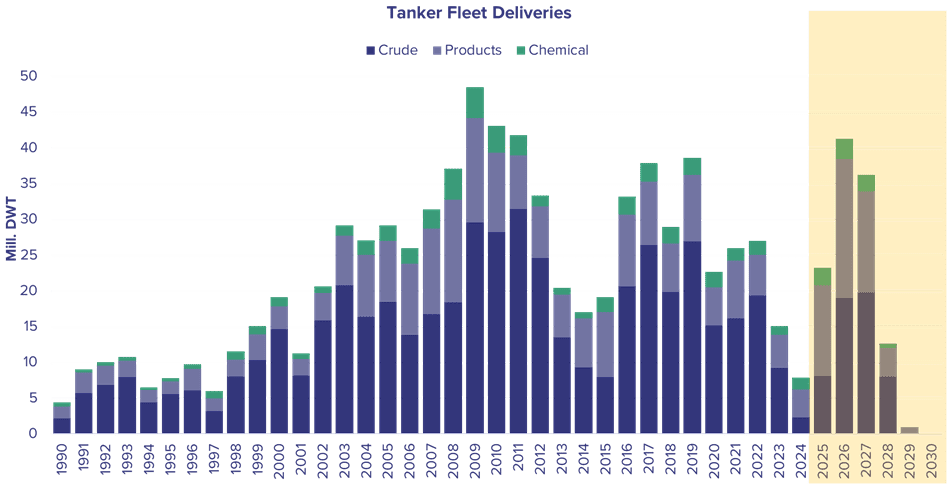

The tanker fleet is particularly noteworthy for 2025, and beyond. Across all three major broad-brush segments (Crude, Products & Chemical Tankers) the delivery schedule is significantly increased for this year, relative to the very light schedules seen across 2023/24. The total deadweight carrying capacity (dwt), across all three segments, scheduled to be delivered in 2025 is approximately 23.2m dwt, a touch higher than the total deliveries of 23m dwt seen across 2023 and 2024 combined. Just over half of these capacity additions are being delivered in the coated product tanker segments, which is seeing the largest delivery schedule for 2025. The crude tanker delivery schedule is less severe during this year, with the 8.1m dwt scheduled still below the 9.3m dwt delivered as recently as 2023. A much lighter VLCC schedule (with only 6 scheduled this year) is helping to limit capacity additions for this segment.

The supply picture becomes much more significant heading into 2026/27, with a total of 41.3m dwt and 26.2m dwt scheduled for delivery in each year respectively. Assuming no cancellations/slippage, the 2026 delivery schedule will mark the highest single year of capacity additions seen across the tanker fleet since 2011. Again, the higher deliveries are being significantly driven by the coated product tanker segments, with the peak of scheduled crude tanker deliveries (19.8m dwt in 2027) only being the highest level seen since 2019. Chemical tankers are also seeing consistently elevated deliveries, although less dramatic than the more conventional tanker segments. The peak for this segment will be the 2.8m dwt of capacity additions scheduled for 2026, the highest seen since the 3.7m delivered in 2010.

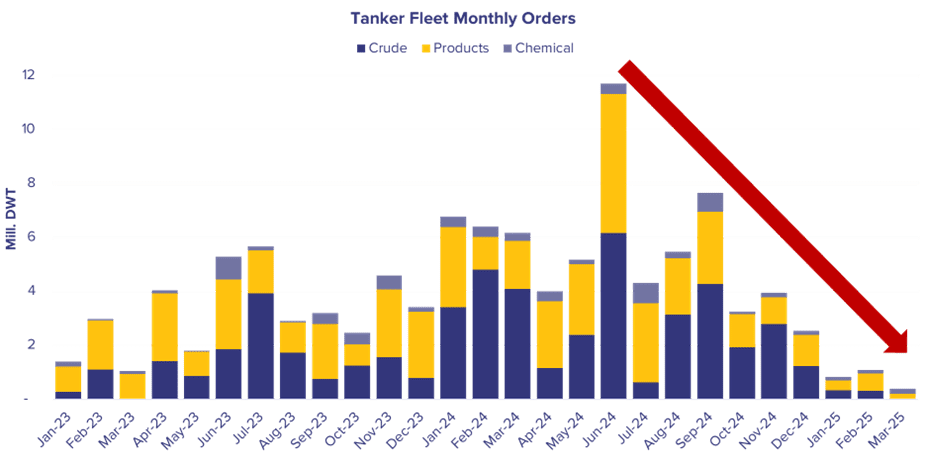

The elevated deliveries scheduled for the near-medium term is on the back of a swathe of new orders being placed across 2023/24. Across the two years combined, a total of 105.9m dwt of tanker capacity was ordered, roughly equivalent to 15% of the currently trading fleet capacity. However, the latter half of 2024 and early 2025 has seen a significant reduction in the pace and scale of new orders. With newbuild pricing still elevated and limited incentives for yards to trim pricing given well-stocked forward books, coupled with remaining uncertainty around propulsion and a delivery window approaching end-decade, notwithstanding the US administrations policy proposals to target Chinese built tonnage, the incentives for placing tanker orders are slightly trickier than in previous years. With many of these factors likely to remain in place for the foreseeable future, this may herald a reduced level of contracting through 2025, helping to limit further significant increases in the delivery schedule.

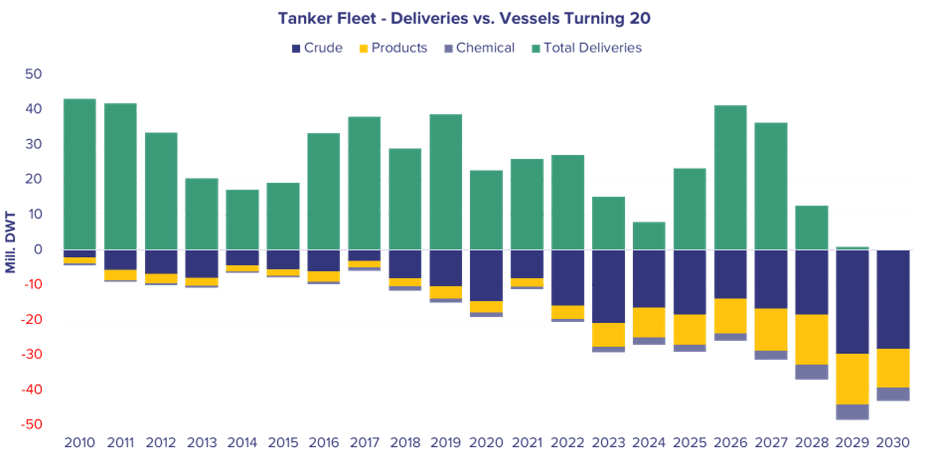

At the same time, the existing fleet continues to age, and age rapidly over the next few years. For 2025, the tanker fleet capacity slipping over 20 years of age sits at 29.1m dwt, comfortably outweighing the 23.2m dwt of new capacity being delivered. Whilst new tonnage will help reverse this trend in 2026/27, as the market approaches the end decade, huge swathes of tankers tip into this overage category. In 2029, as a stand-alone example, a total of 48.5m dwt turn over 20 years old.

Not only will this help the tanker market to absorb the already increasing deliveries scheduled but also create significant requirements for further fleet renewal longer term, particularly in light of the ever-increasing focus and demand for younger, efficient and less carbon intense tonnage continues to grow.

For more information on this topic please do reach out to us at [email protected].