Understandably the focus in the tanker market has been on the demand side as trade flows changed profoundly over the last couple of years, due to wars and geopolitical tensions that increased its influence on shipping dynamics over the period. The supply side of the market until recently was regarded as an uneventful affair, although its influence on the future market dynamics is equally important.

Since the beginning of last year, we started witnessing some renewed interest in the newbuilding orders. That interest further amplified in the last 12 months or so, as the newbuilding orders have grown significantly. Between January and May 2023, almost 14 million dwt was contracted in total. To illustrate the strengthening of the interest in the newbuilding vessels, 2023 ended with 44m dwt of newbuilding capacity, which means around 30 million dwt of orders was added from June towards the end of the year. The yearly totals are strong but not spectacular, having in mind a low level of newbuilding orders post 2015, which averaged just below 20 million dwt on yearly basis. However, the momentum that was noticed in the second half of 2023 have continued throughout the first half of 2024, as total capacity on order between January and June 2024, amounted to 28m dwt, and if the pace of the newbuilding orders continues this year, those are expected to outstrip the total orders of 2023.

Despite the fact that the pace of the newbuilding orders remain similar between the years, there are some differences as with regards to the vessel segments and sector dynamics. Incentivised by strong earnings, product tankers orders dominated the market during 2023, with 55% of the total dwt tonnage on order, which is naturally even more amplified in the number of ships due to their lower average size. In total around 24.5m dwt of product tankers capacity was ordered during 2023, which is the highest level of orders since 2006. The newbuilding orders in this segment were dominated by the orders in MR and LR2 sectors, with 155 and 129 ships ordered respectively. The pace of newbuilding orders continued during 2024 for the MR sector, as 87 units were ordered so far this year, while interest in the LR2 sector softened with 34 units ordered. Interestingly, there has been some renewed interest in the LR1 sector with 16 units ordered during 2023 and 21 further units ordered in the first half of this year.

On the crude oil tankers side Suezmaxes saw the largest number of the newbuilding orders since 2015 last year, when 66 units were ordered for the sector with single digits deliveries during 2023 and 2024. What has been different so far this year for the crude oil segment is that newbuilding orders switched to VLCCs as 39 units were ordered in the first half of the year, which is already the highest number of VLCCs on order since 2017, when 55 units were ordered for the whole year. Chemical tankers orders picked up, with 2023 orders being the highest since 2015, although compared to other sectors, in particular product tankers, the orders remain relatively modest.

The ratio between newbuilding orders and active orderbook currently stands at a respectable 19% for product tankers and 7% for crude oil tankers. The higher ratio for the product tankers is particularly supported by LR2 orders, as the ratio for that fleet stands at 38%. Despite the stronger newbuilding orders, the ratio is still much lower than some recent historical highs.

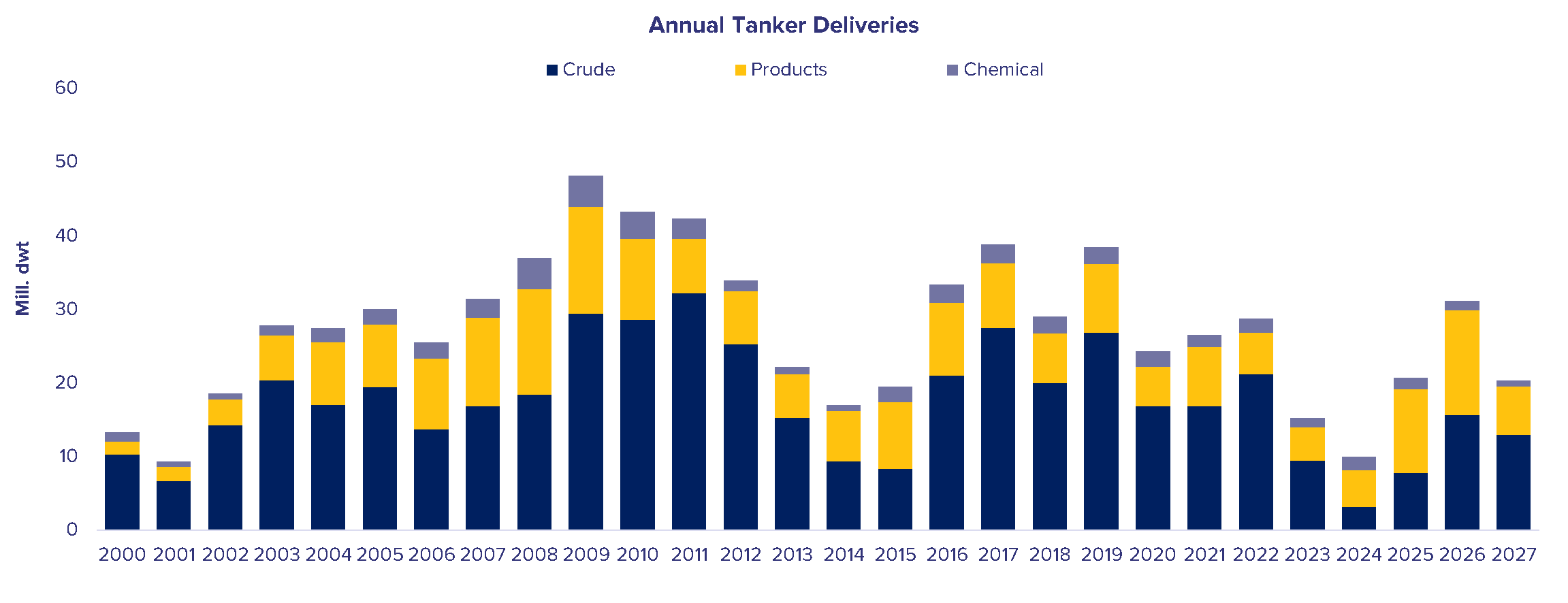

Newbuilding deliveries this year and next are still expected to be subdued despite the recent orders, with the total capacity currently showed to be peaking during 2026, when slightly more than 30m dwt is scheduled for delivery, which is the highest levels since 2019 when 38m dwt of capacity was delivered. Product tankers fleet is expected to have much stronger growth relative to the size of the fleet as the 2026 deliveries are expected to be the highest since 2009, with 14m dwt currently scheduled to be delivered. On the other hand, the crude oil tankers fleet is also anticipated to peak and grow by around 15.6m dwt of capacity in 2026, but that growth is very modest by historical standards, despite recent newbuilding additions.

Current supply tightness can be reflected in the fact that demolition levels remain very modest despite high demolition prices, as the older units are able to trade “off market”, due to recent trade flows dislocations and geopolitical tensions. Having in mind that most of the tanker fleet are ageing rapidly, with the number of units tipping to 15 years of age growing since 2023, the recent additions are going to bring limited relief to the tightening supply, particularly for crude oil and chemical tanker fleets. Limited yard capacity will mean that further newbuildings deliveries are going to be coming post 2026/27, while questions around propulsions systems due to changing environmental regulations and strong newbuilding prices still continue to deter some owners from ordering new vessels. The above factors indicate that the fleet tightening is expected to continue over the next few years, with some exceptions for the product tankers fleet.