Donald Trump has been elected as the 47th President of the United States, with the Senate also set to return to Republican control. President Trump to be inaugurated on 20th January 2025, meaning no fundamental changes to policy until early next year. Throughout this article we outline some of the key themes of a Trump Presidency that could impact the Tanker market going forward.

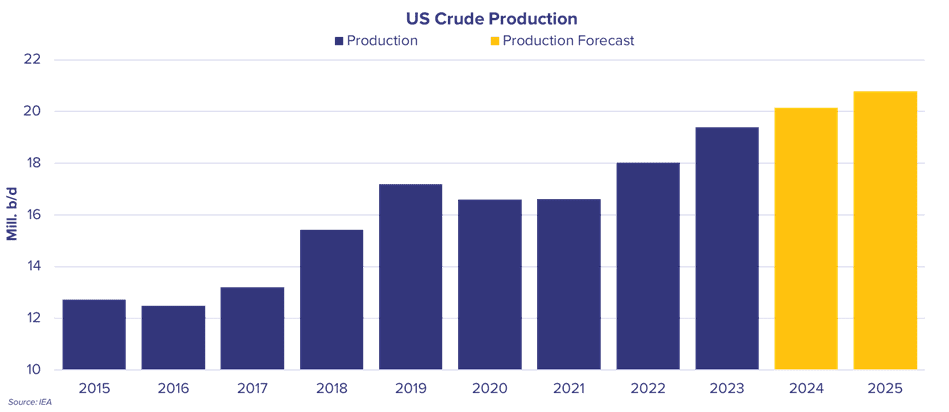

US crude production continues to grow at a strong pace throughout 2024/25. Production is expected to increase by 0.63m b/d in 2025, which whilst a lower pace compared with growth across 2022/23/24 still offers upsides to the tanker market. The growth of US crude exports offers significant support to tankers overall, with much of the share of business taken by VLCCs and Suezmax tonnage, often on longer haul business, which offers significant tonne-mile upside to these segments over the near term. This narrative, with production being driven predominantly by market forces, rather than significant political will, means that the growth story into next year will be holding regardless of White House policy.

Energy security and promotion of domestic energy production will remain a key focus under the Trump administration and there have been longer-term statements (“drill, baby, drill”) throughout the campaign showing Trump has a desire to promote the domestic energy industry. These policy focuses can help have an impact on longer term projects, rather than immediate seaborne volumes. Increased drilling and new leases can help the long-term production outlook for US energy production, whilst in the more medium term offer potential areas for new employment of offshore O&G vessels.

The US refinery industry, as with other regions that have an ageing refinery base, is expected to see capacity declines over the medium/long term. The US is expected to see refinery capacity decline by around 400,000 b/d by 2030 (according to IEA). There could be a range of policies to unpack going forward that could have an impact on the US refined products market.

President Trump is likely to be more naturally hostile towards greener fuels and energy sources. This can range from similar exemptions for smaller refiners from biofuel blending requirements as was seen during Trump’s first term in office, hurting bio demand, whilst helping to increase demand for more traditional feedstocks. Any trade tariffs imposed as part of wider protectionist measures could impact imports of feedstock, and products that support production, potentially putting downward pressure on imports and upward pressure on domestic prices.

Trump may also seek to repeal Electric Vehicle tax credits, which could help to trim demand for and uptake of electric vehicles in the medium term, offering support to gasoline demand over the same time horizon.

President Trump can have significant impact on trade policy, but there remains a significant number of unknowns going forward. OPEC+ policy has been driven by hesitant demand growth, with the current position of the organization being the beginning of a phased reversal of 2.2m b/d of voluntary cuts from 2025 onwards (a date that has been pushed back over recent months).

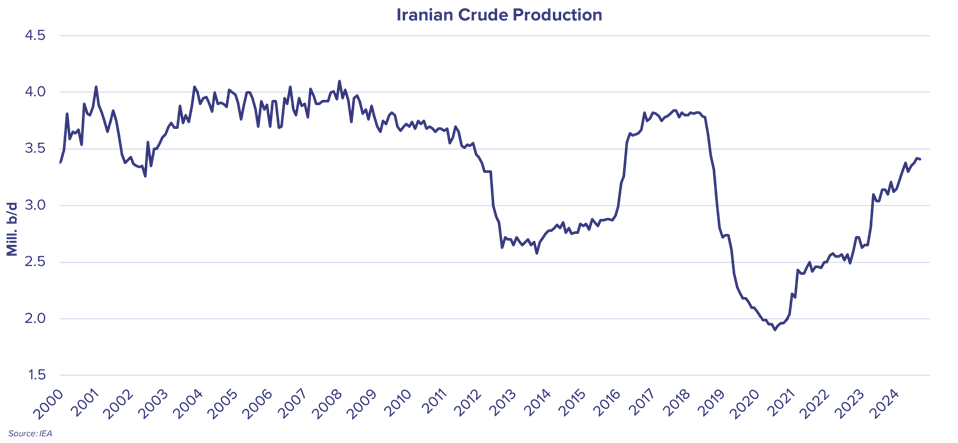

At the same time whilst President Biden has been in power, Iranian crude production has surged. The previous Trump administration dismantled Obama’s nuclear deal and imposed punitive sanctions on Iran, leaving Iranian production at only 2.2m b/d by the date of Biden’s inauguration. Whilst Iran, and Chinese Independent refiners that make up most of the market for the crude, have become more capable of working around the sanction regimes, should Trump adopt a hardline stance in his second term, further pressure could trim Iranian crude exports. In such a scenario, this could further open the door to OPEC to reverse ongoing cuts and fill any gap left by Iran. This would be a significant net benefit to larger crude tankers, as barrels come back to the mainstream, and some older ‘dark fleet’ vessels likely have to be recycled.

The US has been a key part of the Price Cap Coalition and ongoing sanctions regimes against Russia. Likely Trump policy towards Russia remains unclear, but Europe is unlikely to be in any rush to reverse the ongoing embargo, meaning the dislocation of Russian energy is likely here to stay for the time being.

Trump’s relationship with global trading partners, and in particular, China was a defining feature of his previous administration. His administration’s ‘America First’ approach saw the application of tariffs and the stepping back from multi-national agreements. Detailed trade policy at present remains something of an unknown, with Trump having threatened to apply tariffs to international imports (with more stringent tariffs applied to Chinese imports). Whether energy imports form part of this policy could be key for the US refining sector, as feedstock costs could rise, refinery throughput potentially coming under some pressure as higher prices filter through into reduced domestic demand.

A wide-reaching trade war with China could have the impact of directly hurting US crude exports to the country, potentially seeing a reduction in tonne-miles for larger crude tankers. Although it is important to note that US exports to China represent a relatively small share of total Chinese import volumes. Equally, policies that hurt the Chinese economy, which is not exactly exhibiting significant strength at the time of writing, has the potential to trim Chinese crude imports, elongating any recovery in Chinese crude demand, one of the defining factors in a weaker than expected tanker market during the back end of 2024. IG Research will continue to monitor ongoing developments in the US political space in the run up to the inauguration of President Trump and the potential impacts they may have on the tanker market going forward. For more information, please do reach out to us at [email protected].