OPEC+ met today (5th December) for their delayed JMMC meeting and have further postponed the roll-back of 2.2m b/d of voluntary cuts for an additional 3 months. The plans, initially announced in June, have been delayed multiple times in reaction to demand and price weakness over the 2H2024. The reintroduction of barrels is now scheduled to begin in April 2025 and continue through until September 2026.

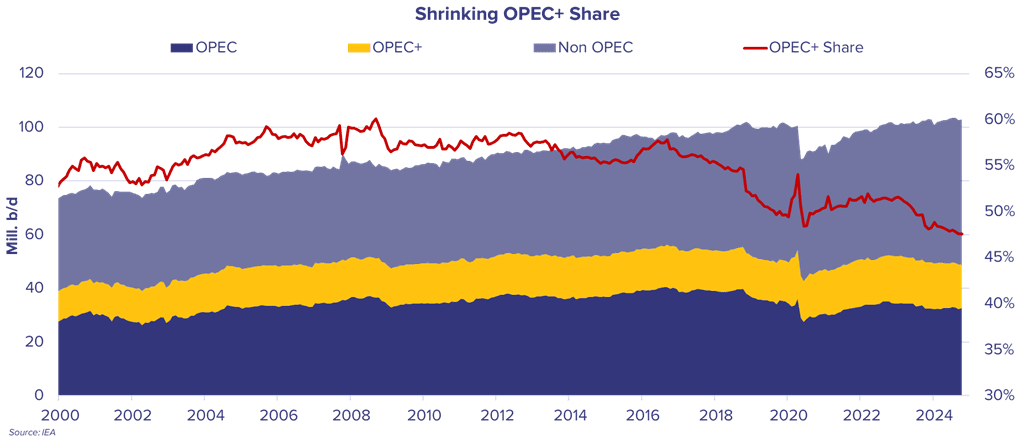

OPEC+ are increasingly caught between a desire to maintain pricing, whilst avoiding further losses to their market share. As non-OPEC producers, notably the US, Brazil and Guyana, continue to grow production, they have been chipping away at the market share of OPEC+, which has consequently dropped to the lowest level in decades.

2025 is likely to bring further challenges to OPEC+ member compliance, with additional barrels coming in from the UAE and Kazakhstan, as investment and projects come on stream.

Iranian officials have been publicly critical of OPEC+ policy, with the organization already having seen Angola defect from the group at the beginning of the year. These pressures will begin to tell in 2025, with the upside to tankers from more barrels coming to market being significant.

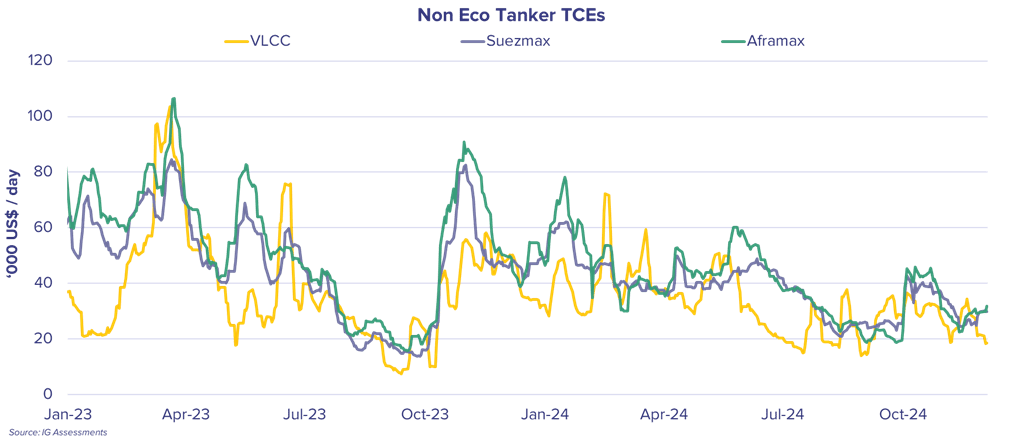

The withholding of significant production by OPEC+ is significantly impacting the tanker market, with VLCCs especially suffering from such significant loss of barrels in the key MEG load region.

Higher than average tonnage surpluses across much of 2023/24, along with substantial ‘off-market’ fixing, has kept freight subdued and elongated a weak summer market deep into Q4. The latest decision from OPEC+ is likely to further elongate this challenging market into 1Q25.

VLCCs have additionally suffered from less upside from the geopolitical driving forces in recent years; with both Russian energy dislocations and Red Sea crises impacting smaller crude tankers more significantly.

When 2025 brings more barrels from OPEC+, along with continued growth of non-OPEC production (1.12m b/d from the Americas alone), VLCCs should see significant upside relative to current levels.

These additional barrels will be coming into a VLCC market, with only 6 vessels scheduled for delivery in 2025, on top of only a single delivery across 2024.

Additional upside could be seen from further US administration targeting of Iranian barrels, with any downside to Iranian production offering a window for more unsanctioned barrels being released into the tanker market.

For more information on this topic and others, please do reach out to us at [email protected].