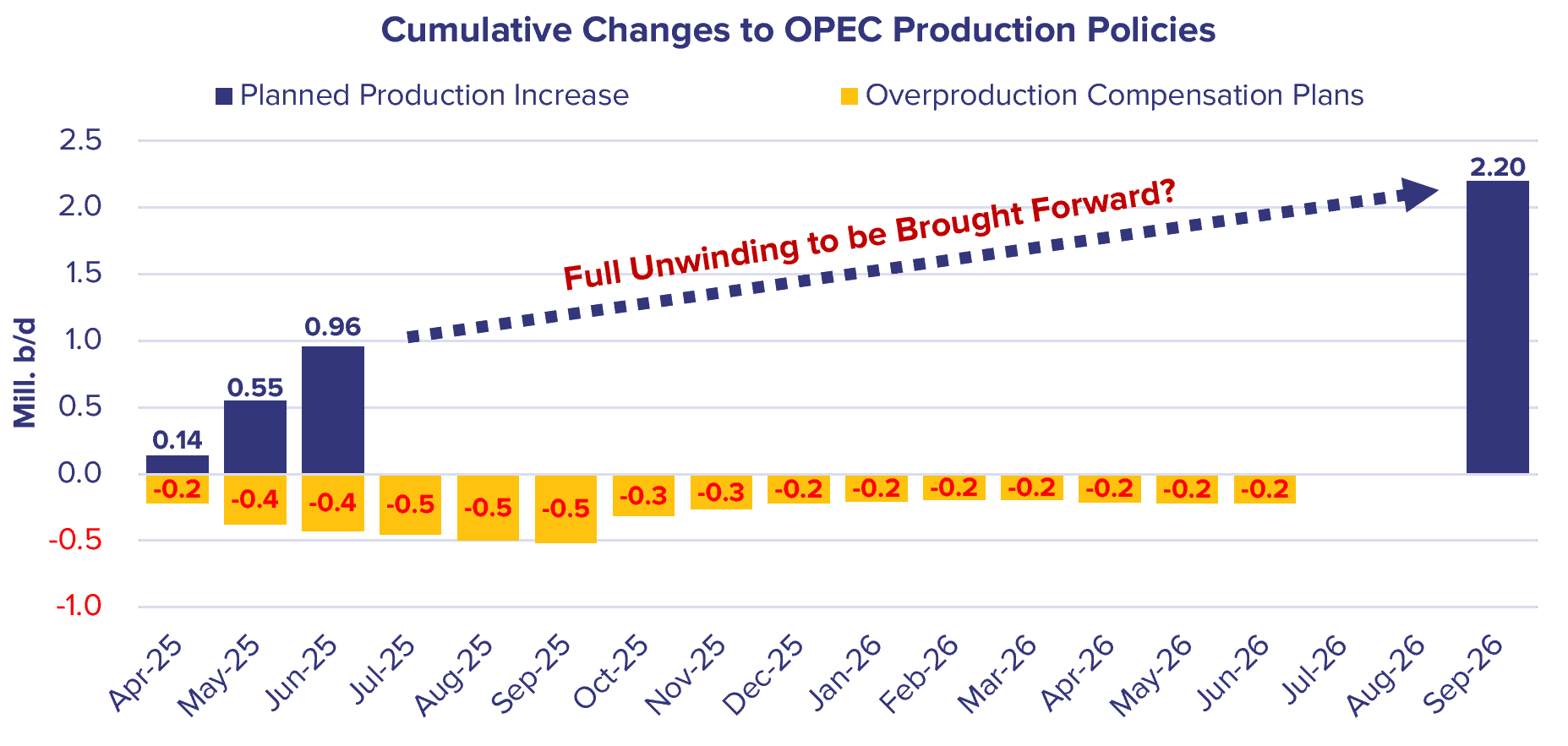

The phased reversal of 2.2m b/d of OPEC+ production cuts was further accelerated on Saturday, with the organisation releasing a further 411,000 b/d into the market for June, on top of the 411,000 b/d already released in May. This brings the total volumes coming back into the market by the end of June to just under 1m b/d, far in excess of any compensation plans. The 8 countries responsible for these changes will now meet monthly to review their plans, opening the potential for sharp policy changes, and potentially the further acceleration towards the final goal of 2.2m b/d back into the market, which was initially scheduled to be completed by end September 2026.

More oil on the water offers significant upside to crude tankers, with increased volumes ex MEG likely to benefit VLCCs most significantly. The policy acceleration can help stave off the usual seasonal weakness that can stalk the market at this time of the year, and potentially offer some more upside to freight levels.

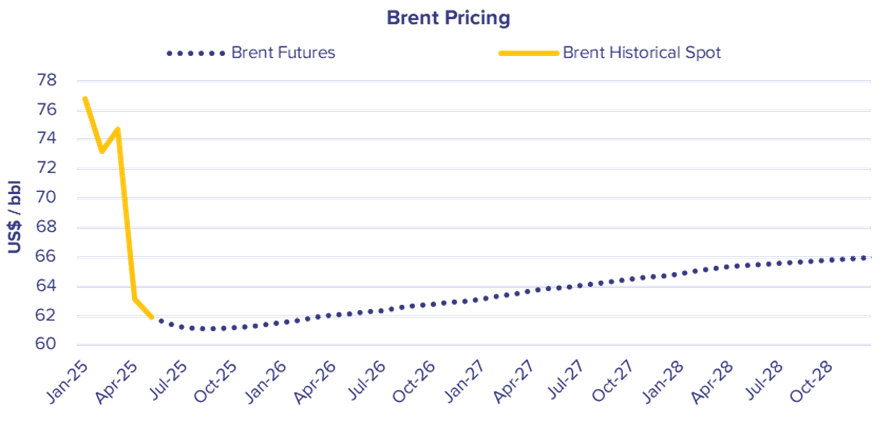

Crude pricing is under pressure, with the lower pricing increasing the likelihood for the opportunistic purchasing of volumes to help restock global inventories, a positive for tanker utilisation. This has been seen in recent weeks, with significantly higher volumes heading into China, a trend that may well continue in a lower price environment. President Trump has also been vocal in wanting to fill the US SPR ‘right to the top’, following releases made throughout the Biden administration.

The reduced feedstock costs can aid refiners and potentially create some upside for clean tankers. The coated segments are likely to also benefit from a stronger crude tanker market, with less incentives for cannibalisation of clean trades with more crude on the water.

For more information on this topic, reach out to us directly at [email protected].