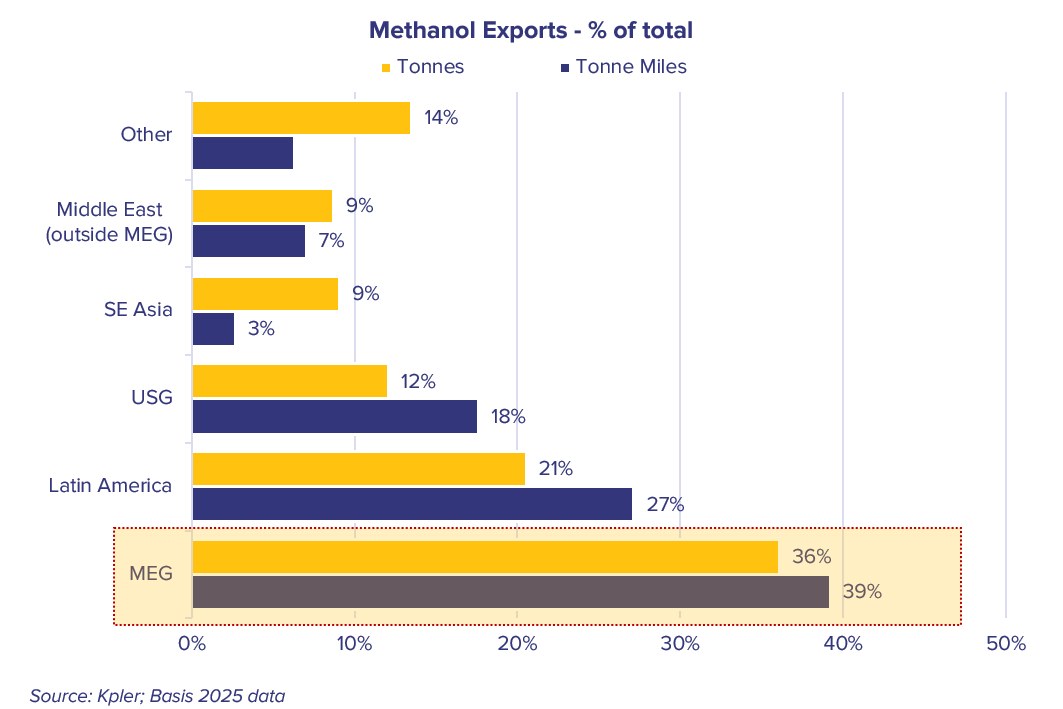

The Middle Eastern Gulf is one of the largest exporters of methanol, benefitting from abundance of the key feedstock such as natural gas. According to Kpler data in 2025 36% of the total methanol seaborne exports passed via Strait of Hormuz. A further 9% was exported from the region outside of MEG. Iran, Saudi Arabia and Qatar are the region’s key exporters of methanol.

The disruption to methanol trade flows is not only coming from the effective blockade of the Strait of Hormuz, but also due to damaged methanol and natural gas production infrastructure. The infrastructure damages, particularly on natural gas fields, production and exporting facilities is likely to have longer lasting effects on the methanol exports as well.

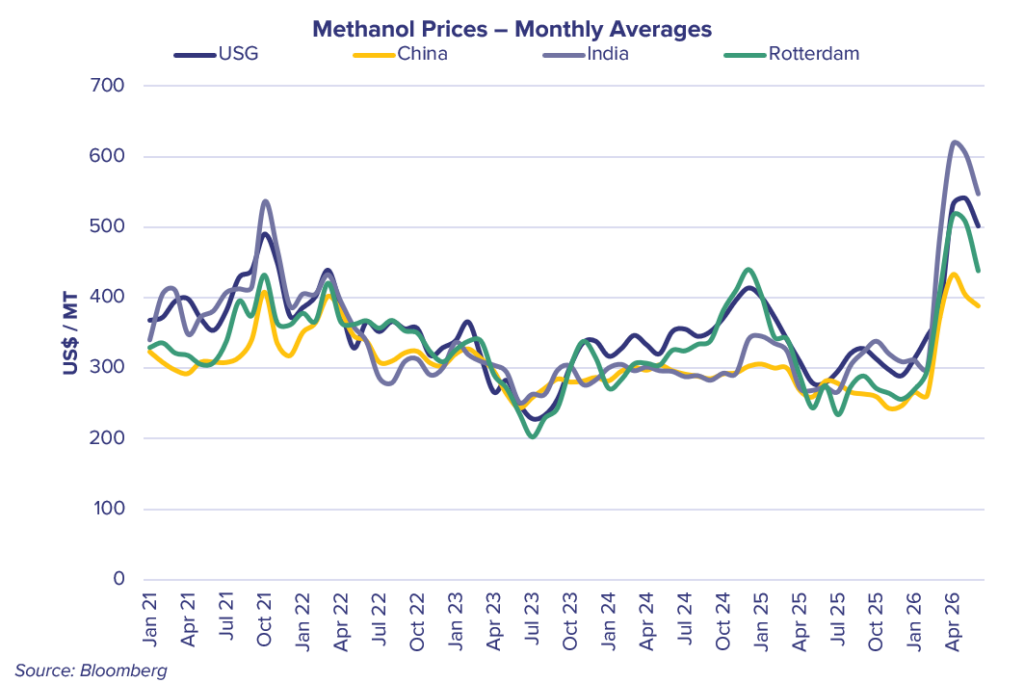

Considering the above-mentioned effect of the trade dislocations and the conflict, it does not come as a surprise that methanol prices moved upwards significantly since the start of the conflict. Notably Chinese prices, although rising, remained well below the levels in other regions.

Prior to the conflict, almost all MEG exports used to target Asian markets. Around 48% of all methanol seaborne imports in Asia originated in MEG. China was a major importer of Iranian methanol volumes, with a significant part of the imports being utilized in the MTO (methanol to olefins) production.

It is worth noting that China has the largest methanol production capacity in the world, with vast capacities for coal to methanol production. Some methanol exports were noted out of China during the last couple of months, with Asian importers trying to ease the pain of the recent disruptions, although the volumes in the grand scale of things are very low.

As expected, methanol production and exports from the US intensified, with May export volumes reaching the highest monthly levels on record. As the exports were mainly targeting further away destinations in Europe and Asia, USG methanol exports helped although only marginally with respects to the overall utilisation levels.

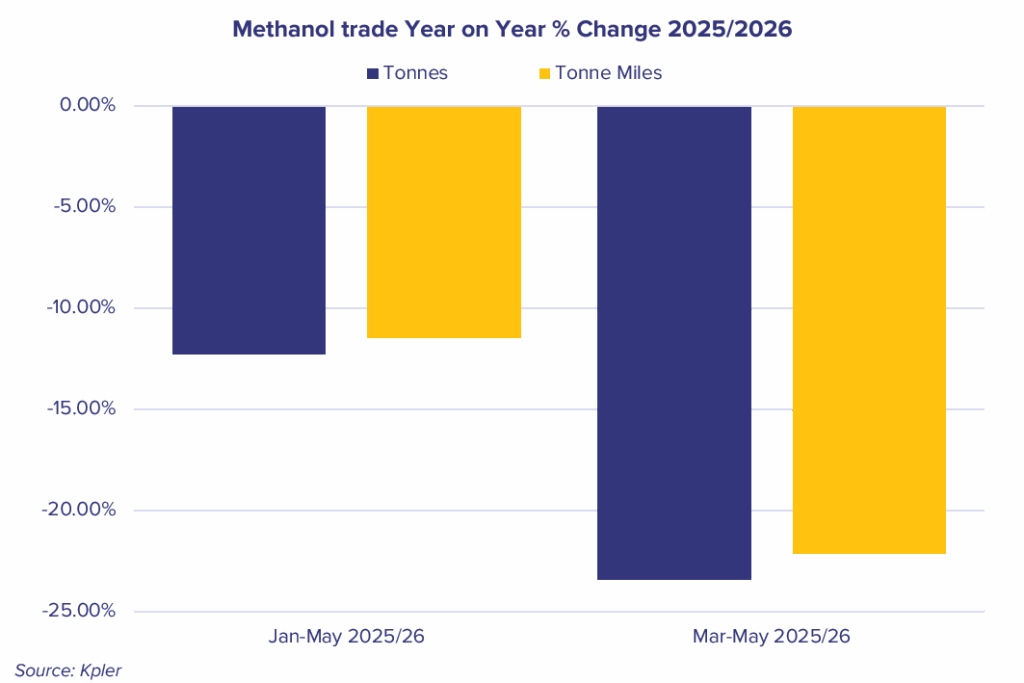

However, it will be very hard to replace the displaced volumes. Both year on year volumes and utilisation levels are down significantly with this year levels for March to May period down by more than 20% for both metrics.