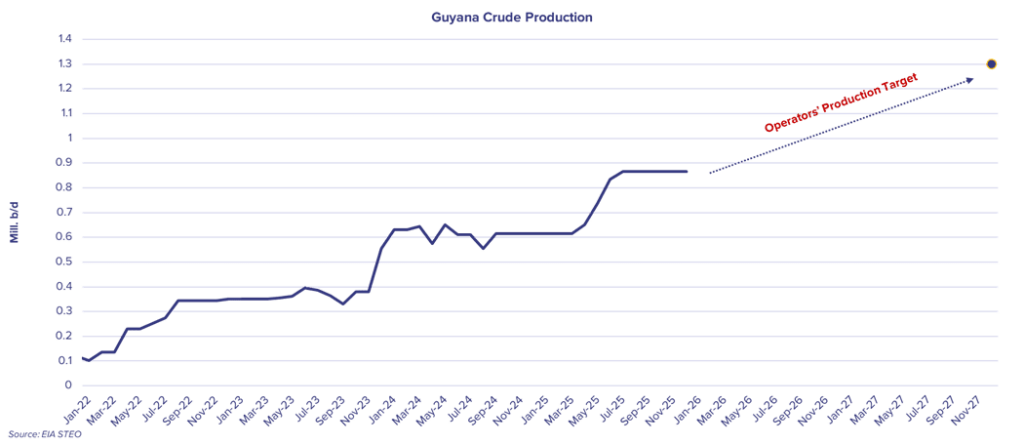

Guyana continues to be a bright-spot for global oil production, with a significant increase in volumes seen in recent years, and further gains expected over the medium term.

A total of 3 FPSOs (Liza Destiny, Liza Unity & Prosperity) are currently in operation in the Stabroek Field, with the operators in the country planning to hit production levels of 1.3m b/d by end 2027, almost double the current level.

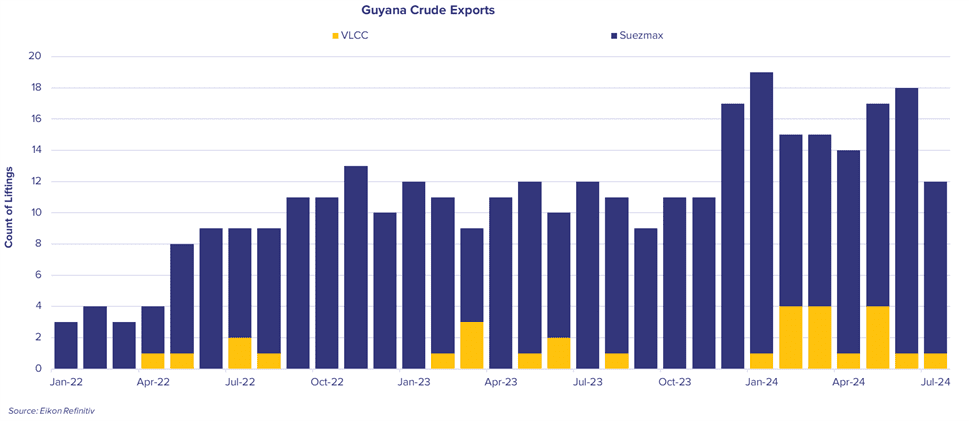

Predominantly a Suezmax business, with 84% of crude exports being carried on the size since the beginning of 2020, there have been increasing volumes lifted on larger VLCC sized stems. Across 2024 to date, VLCCs have accounted for just over a quarter of liftings.

There remains a logistical limit to the extent that VLCCs can cannibalize this business from their smaller cousins, with the larger vessels unable to lift from the Guyanese FPSOs during winter months due to period of adverse currents. As shown in the data alongside, there has never been a VLCC lifting crude in October, November or December months.

With Guyanese crude production growth expected to continue over the coming years and achieve 1.3m b/d during 2027, demand for Suezmax and VLCC tonnage is likely to increase in the region.

So far during 2024, just under 60% of Guyanese barrels have headed Transatlantic into Europe. If the forecasted additional 745,000 b/d expected between August 2024 and end 2027 all head on the relatively short TA voyage to Rotterdam, this would create additional demand for the equivalent of 26 extra Suezmaxes.

With some barrels heading further afield, either directly, or indirectly via the Transisthmian Pipeline, the potential impact on vessel demand could be greater still.

The growth in supply from a single country can therefore go a significant way to absorbing some of the scheduled deliveries over the 2025-27 timeframe and help keep freight comparatively elevated.

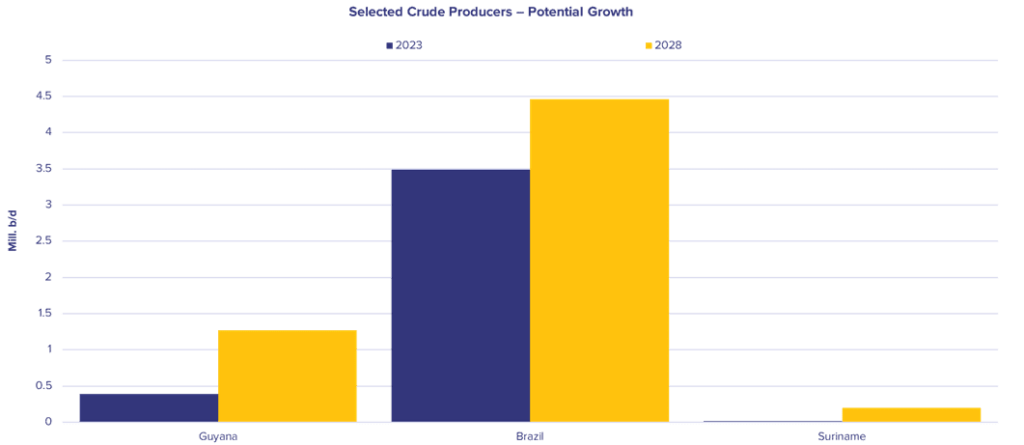

Guyana is by no means the only area of significant growth; Brazilian production continues to go from strength to strength, whilst Suriname is the latest ‘hot topic’ in crude exploration & production.

Petrobras’ latest Strategic Plan (2024-28) highlights a total of 14 FPSOs planned/scheduled to begin production, and with the continued involvement of several NOCs and Oil Majors, production is forecast to increase significantly across the medium- and long-term horizons. By 2028, the IEA forecasts Brazil to see production hit just under 4.5m b/d, an increase of almost 1m b/d on 2023 levels.

With the long-haul export nature of many Brazilian barrels, such growth can expect to contribute to the tightness of the larger crude tankers for the foreseeable future.

Suriname, a country that has been producing small volumes of crude for decades, has seen recent significant offshore discoveries create the potential for production and export growth over the longer-term time horizon.

The earliest likely project, a consortium including TotalEnergies and APA Corp, is heading towards a Final Investment Decision by the end of 2024, with a 200,000 b/d FPSO hull already secured. Subject to the FID, production of this particular project is scheduled to commence in 2028.

With an estimated 2.4bn barrels of recoverable oil reserves, whilst it remains early days for Suriname production growth, there remains significant possibilities over the coming decades for further growth and therefore additional tanker demand.

For further information, do reach out to us at [email protected].