October saw the 1998 built Suezmax MT ‘Alana’ recycled in Chattogram, Bangladesh, for a reported US$ 570 / ldt. Notwithstanding the considered ‘Total Loss’ of the Aframax MT ‘Pablo’, a vessel that had earlier suffered a tragic explosion onboard, this Suezmax demolition is the first such activity seen in exactly 12 months. It is a sign of how rare tanker, and especially crude tanker recycling is, that it warrants a closer look at the demolition activity, demolition markets and the dramatically shifting age profile of the currently trading tanker fleet.

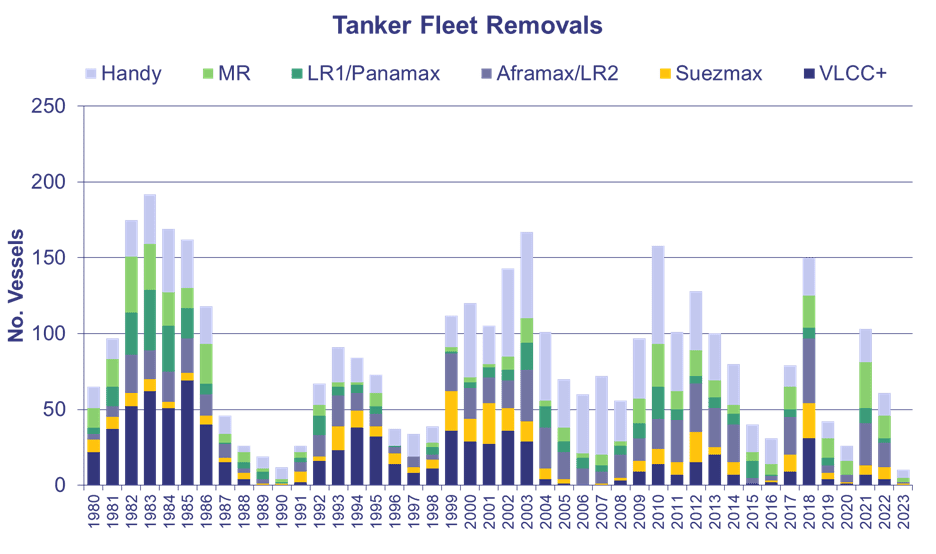

It is no secret to anybody following the tanker markets that recent years have seen a dearth of recycling, as the lucrative grey and dark fleets have provided the opportunity for continued trading of vessels that may in historically normal markets been destined for far earlier recycling. Older tonnage has been changing hands for significantly elevated pricing, with the current value of a 15yr old Suezmax sitting around the US$ 42m level, far in excess of historical norms, although having corrected downwards in recent months from the exceptional highs of earlier this year. These factors have unsurprisingly kept older tonnage well away from the demolition yards.

Any recycling in the past 12 months have been largely amongst the smaller vessel segments, with 4 MR’s and 5 Handies being demolished, along with some additional scrapping (29 vessels) in the sub 25kt vessel segments. The average age of all vessels demolished over the past 12 months sits at just over 33 years of age, a further indication of the sheer lack of willingness to recycle vessels unless in extreme circumstances.

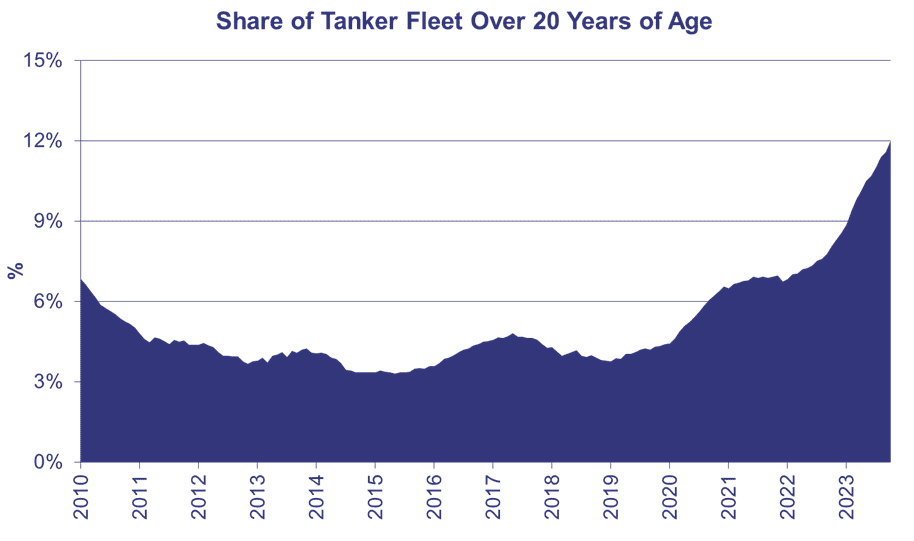

The net effect of limited recycling has been a quite dramatic increase in the pool of tonnage that sits above 20 years of age. At present, 12.3% of the overall tanker fleet is over that age (13.2% and 10.1% for crude and products fleet respectively). This figure represents the highest fleet size share of older tonnage seen in almost two decades. By comparison, in January 2019 it was 3.9% of the fleet that was over 20 years old. With such a limited delivery schedule for 2024, and to a lesser extent for 2025, the age profile of the fleet will alter significantly over that time period. If we take the VLCC’s as a prime example, at present about 12% of the fleet sits over 20 years of age. With only 6 vessels being delivered in this segment across the entirety of 2024/25 the new tonnage entering the fleet is going to be dramatically outweighed by the 57 vessels tipping over into this ‘overage’ category of 20+ years of age over the same time period.

In any ‘normal’ market, especially with demolition prices remaining high, this seismic shift in age profile would likely precipitate a substantial period of fleet renewal and recycling of older tonnage. However, with the wider tanker market enjoying much higher returns at the beginning of a much anticipated winter market and expectations of a healthy couple of years, along with the exports from Russia and Iran still offering a lucrative haven for older tonnage, there is unlikely to be a large rush in vessels heading to the beaches.

However, the market is building up a substantial pool of demolition candidates, which points ultimately towards some likely substantial recycling over the coming years.