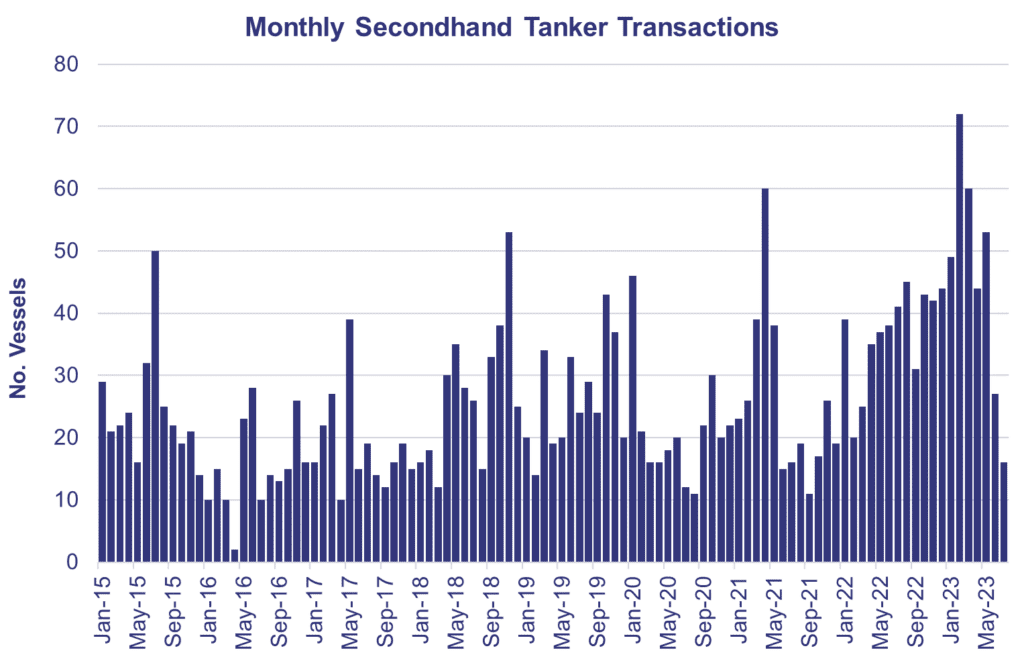

Equally the secondhand tanker market has been exceptionally frothy, especially and busy during the latter part of last year and earlier this, particularly as the tanker market heated up and older second-hand tonnage became increasingly sought after for trading lucrative Russian trades. In February 2023 we have recorded a total of 72 tankers sold in the secondhand market, the highest level ever reported in the market, which was then swiftly followed by March 2023, where the second highest level of transactions were reported, 60 in total.

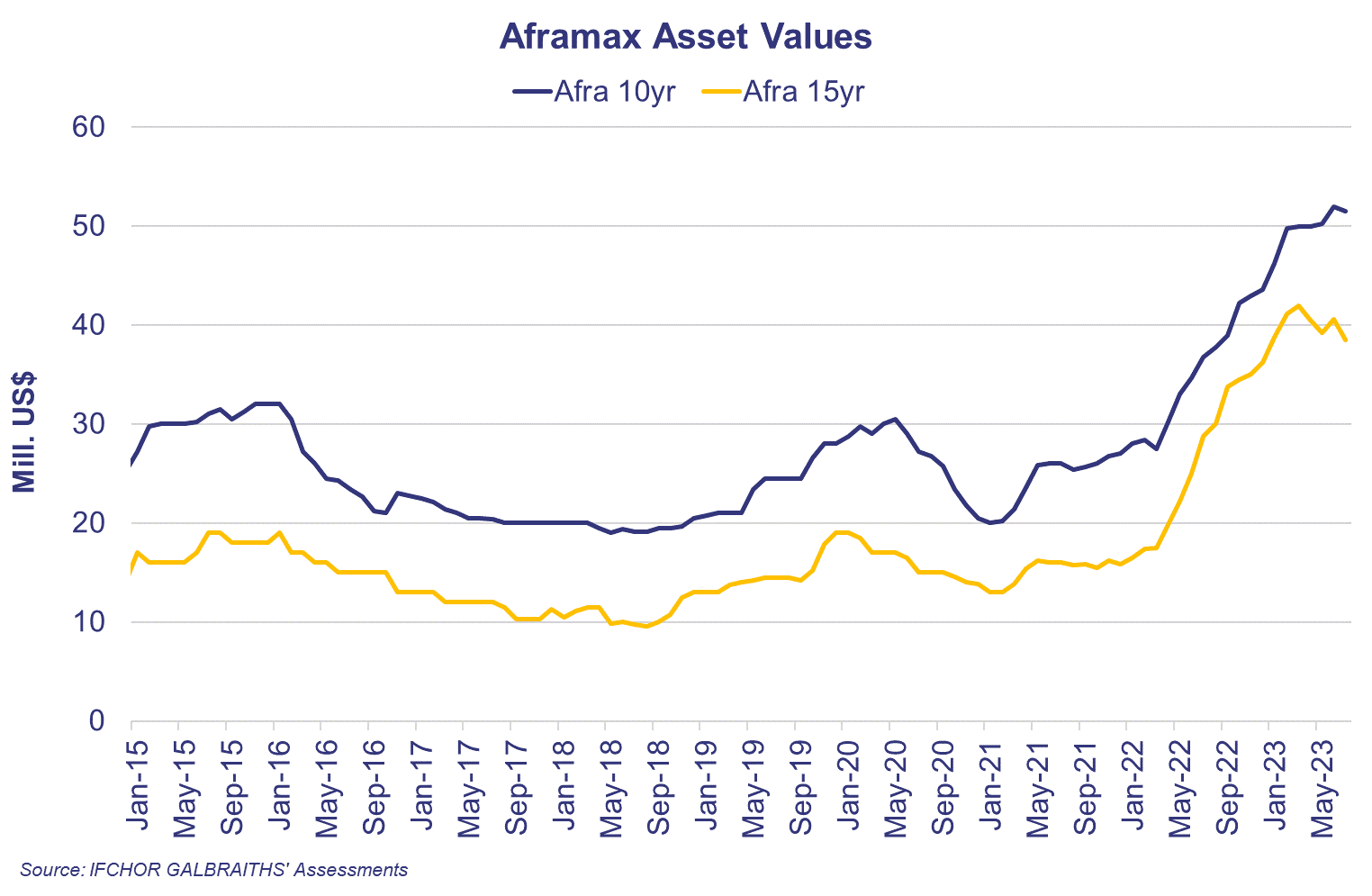

On the back of this spike in vessel demand, tanker asset values have ballooned. In March of this year, a 15yr old Aframax was priced at US$ 42m, a near 230% increase in the space of two years, and only marginally below the newbuild price of an Aframax back at the beginning of 2021 (US$ 45m).

Since these peaks earlier in the year, interest in secondhand tankers have waned, with July only seeing a total of 16 transactions reported. On the back of this reduced activity, pricing has begun to drop back from the peaks of earlier this year, with the current value of a 15yr old Aframax sitting at US$ 38m, about 10% below the peak. Much of this is a reflection of the transition of this older tonnage into new ownership for the changing trades, and this phase looks to have completed for the time being.

In respect of this market for older tonnage, a close eye should be kept on the developments of Russian crude pricing, which has breached the Price Cap values in recent weeks, resulting in a migration of tonnage away from those trades and back into the wider market-based fleet. This migration has been reflected in the increased tonnage availability in the Med especially, and the declining rates seen across these markets. It will be interesting to see how the chartering market develops with charterers taking differing views on a vessel’s trading history. The slowdown in transactions may lead to those owners looking to offload older tonnage finding weaker buying interest and therefore adding further downward pressure on pricing in this age bracket.

That being said with a strong outlook for the spot market going forward, despite current seasonal correction, owners may choose to hold on to tonnage in the short term if values were to correct much further with the last 18 months having given owners significant cash buffers.

Where there is more uncertainty is in the medium term as environmental pressures and associated costs to running older vessels are likely to increase the pace of tanker deletions. With newbuilding availability now extremely limited even in 2026, an increase in scrapping will give further confidence of a lengthy period of positive earnings.