The conflict in the Middle East has caused a huge dislocation and scramble for energy products. Much focus has been placed on the huge share of crude that is trapped within the MEG; 32% of global seaborne volumes and approximately 37% of crude tanker tonne-mile demand, both basis full year 2025 data.

Clean Petroleum Products (CPP) are hardly insulated from this crisis. Based on 2025 volumes, around 16% of global seaborne CPP volumes and 23% of global CPP tanker demand transited via the Strait of Hormuz. Whilst the contagion spread and continues to spread globally, Asian buyers were uniquely impacted as large share of their import slate, especially for crude feedstock, was taken from impacted MEG exporters.

The Chinese government also reacted quickly to the tightness in feedstock and threat to CPP flow, with initial guidance around limiting CPP exports, subsequently tightened to fully restrict CPP exports and cancelling of ongoing export cargo negotiations.

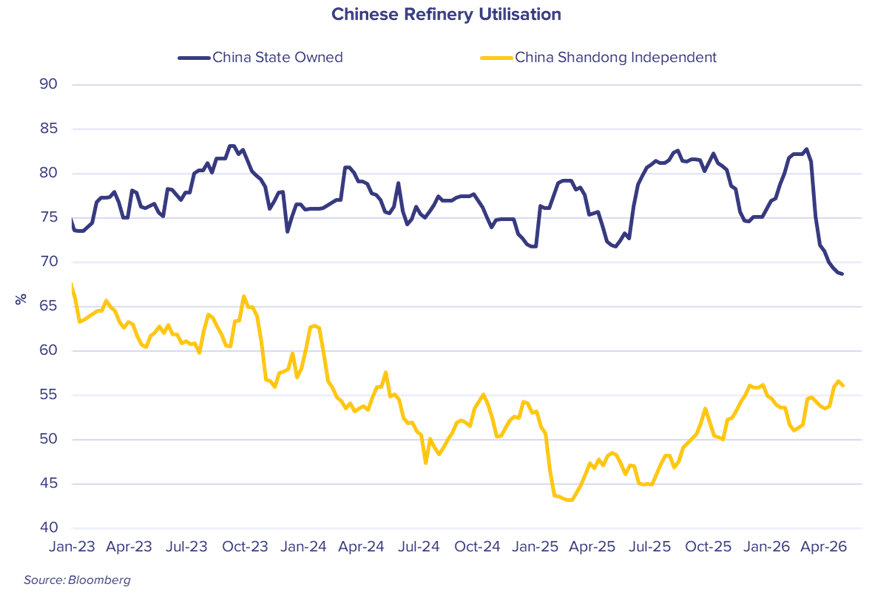

This tightness within refined products in the region has been emphasised by the large increases in petroleum pricing, refining margins and by the reaction of refiners. State-owned refineries especially dropped throughput and utilisation significantly, as their main source of feedstock was jeopardised. Chinese state-owned refinery utilisation has dropped to just under 70% at the time of writing, the lowest level seen since 2022.

Whilst Chinese CPP export volumes sit comfortably behind those of South Korea as the region’s largest exporter, the country exports significant quantities of refined products, a total of just under 30m mt across 2025, with the largest share of which being Jet (14m mt) and Gasoline (9m mt).

Chinese exports are largely an intra-regional narrative, with only limited quantities of products heading further afield. Approximately 83% of Chinese refined product exports remained within the Asian/Australasian region, with the vast majority of cargoes being lifted on MRs. With lower refinery utlisation and the effective ban on exports, volumes of CPP ex-China during April dropped to near record low, with a 43% decline relative to the same month last year, stripping regional MRs of some of their cargo base.

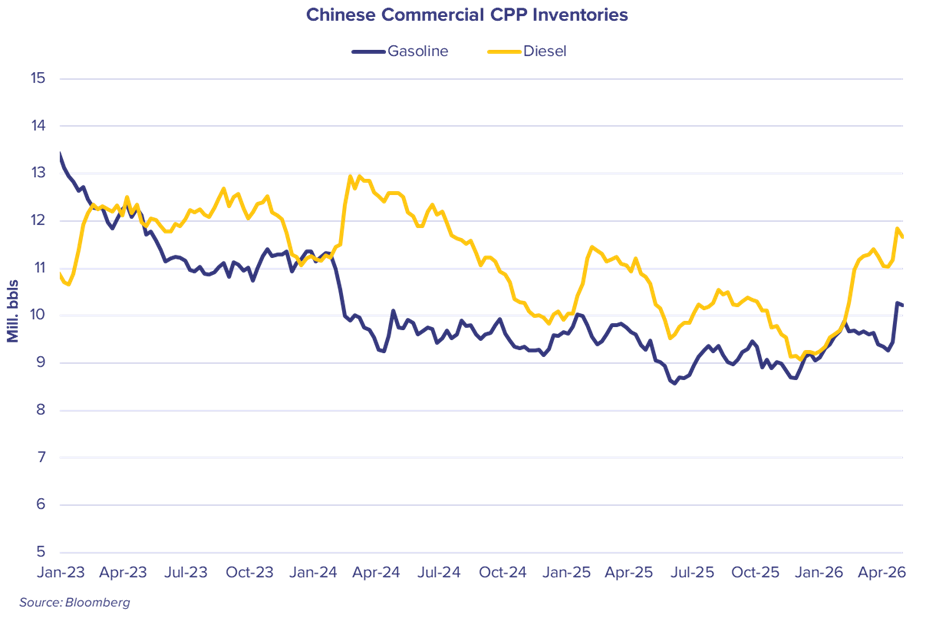

However, in the past week reports suggest that the Chinese government is relaxing the export ban, with targeted relaxations allowing export of certain refined products to key regional buyers, many of whom are reported to be experiencing severe supply shocks of key fuel, most notably, jet. China is likely confident enough to pursue this change of policy, given their own stockpiles of CPP have remained robust over recent weeks, as a combination of the government policy and relatively healthy ‘independent’ refiner’s utilisation helped to insulate Chinese inventories from the worst of the drawdowns seen elsewhere.

With the relaxing of the export policy, this should offer some support to MRs in the region, especially as buyers of Chinese barrels are likely to scramble for these freshly available cargoes and fix far forward in order to secure the much-needed barrels. However, the export ban had also created a significant uptick in long-haul barrels coming into Asia, both for MRs and amongst larger LR1/LR2 segments, with tonne-miles being supported by a significant jump in volumes coming from the Americas during March and April. With Chinese policy still in its early days, there remains plenty of moving parts, but a reduction in these longer-haul barrels could see MRs benefit regionally, at the expense of some of those longer-haul trades.

It is not only the CPP markets that have been in the Chinese administration’s crosshairs as a result of the crisis in the Middle East. Reports suggest that from 1st of May, the export of sulphuric acid will be restricted in order to maintain domestic supplies. China was the top exporter of sulphuric acid last year and the effect of the ban is expected to be felt in chemical, fertiliser and metal production. We will closely monitor development and impact on the chemical and stainless steel tanker markets.

For further insights, contact [email protected].