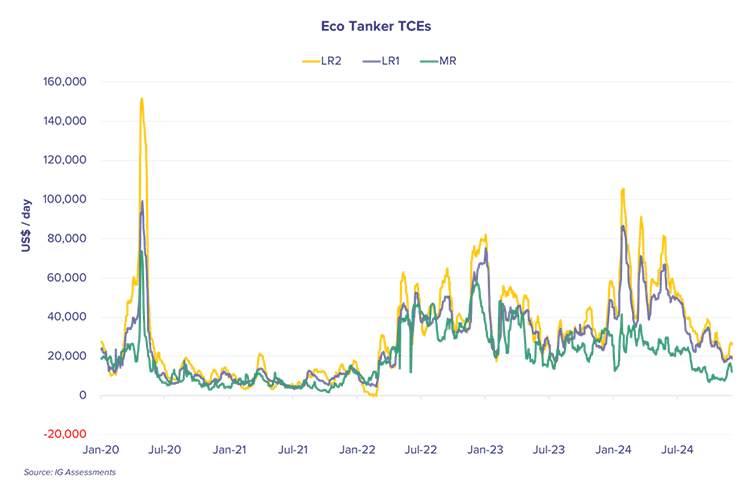

After such a healthy market in the 1st half of 2024, clean tankers have endured a challenging early winter market, with freight and earnings being under significant pressure. At the time of writing weighted average basket earnings sit at US$ 26,000 / day, US$ 19,000 / day and US$ 12,000 / day for eco LR2, LR1 and MR tankers respectively.

Whilst the challenging market has by no means been unique to clean tankers, with crude also seeing a much weaker than anticipated winter period, the slide seen relative to the 1H2024 has been far more pronounced on the CPP side. Average eco earnings for a VLCC have slid by around 30% from 1H2024 to 2H2024 at the time of writing, whilst MRs have seen the comparable average drop by 47%. This collapse has partly been exacerbated by the substantial spikes seen earlier in the year, as CPP tankers, especially heading East to West were dramatically impacted by the longer voyage times to avoid the crisis in the Red Sea.

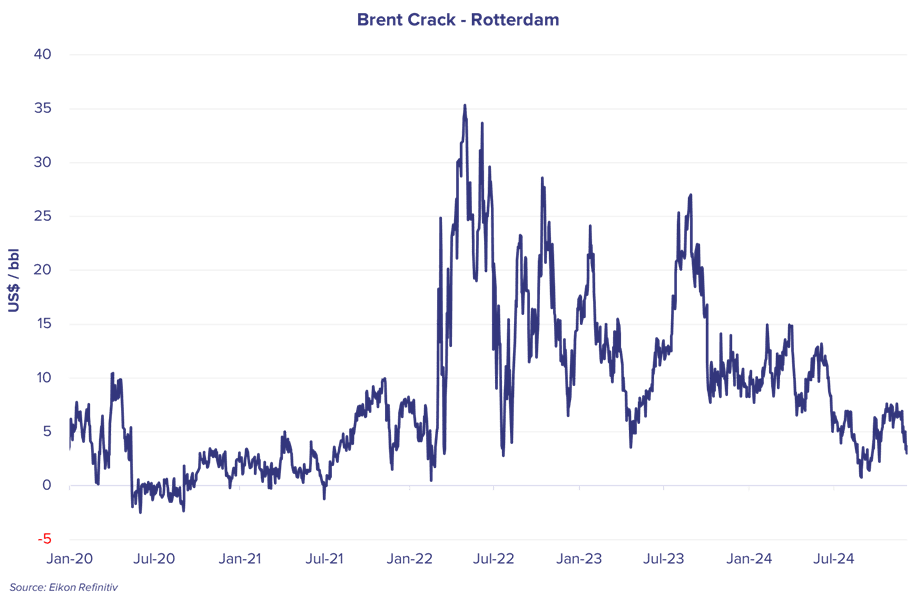

There have been some additional contributing factors to the clean market weakness over recent months. Refinery margins have been under pressure, as demand growth faltered throughout much of 2024. The Brent crack, slipped to just under US$ 1/bbl at the end of August, and whilst it has recovered over recent months, remains far below levels seen in much of 2022/23. This has helped contribute to lower reported throughput levels, with the IEA reporting an October low point of 81.8m b/d, as economics run cuts came on top of seasonal refinery maintenance, helping to pressure cargo availability for CPP tankers.

2024 has seen a developing trend of large crude tankers jumping away from weakness in their conventional markets and ‘cleaning-up’ to lift clean cargoes. This has helped further trim the cargo availability for CPP tankers, with each VLCC choosing to enter this trade, taking away the equivalent of 3 LR2 cargoes. The now weaker CPP market, coupled with long-haul demand growth from crude tankers from significant non-OPEC Americas cargo growth in 2025, should help limit further cannibalisation of clean cargoes, especially once the now additionally delayed OPEC barrels start coming back into the market from April 2025 onwards.

There remain some headwinds into the beginning of next year, with the tanker market seeing an uptick in deliveries relative to the very low-point of 2024, along with some concerns still present around the health of the global economy. Overall, global oil demand is expected to increase by a touch under 1m b/d across 2025. However, a key driver for CPP tankers will be a very significant swing in refinery capacity between East and West of Suez. The IEA expects net nameplate capacity in the Atlantic basin is expected to shrink by 207,000 b/d, with additions of 450,000 b/d East of Suez, offering some potential significant East to West flows throughout 2025. This should offer some upside to clean tankers, with the larger sizes in particular being utilized on longer runs.