IFCHOR GALBRAITHS (IG) is a significant player in chemical and biofuel broking, opening a desk in 2022 in Bergen, expanding with further offices in Houston, Dubai and Geneva in 2024. As tightening fleet supply, longer trade routes and the rapid rise of biofuels, biofuel feedstocks and ethanol cargoes reshape the market, IG brokers are more than just transactional shipbrokers. They increasingly act as technical advisors, risk managers and market strategists — driven by the demands of sophisticated owners and freight traders.

The latest Annual Chemical Report from IG’s research team highlights the scale of change underway. Global chemical seaborne trade continues to grow steadily, supported by rising volumes and diversification, particularly in biofuel and feedstock grades. At the same time, fleet dynamics are tightening.

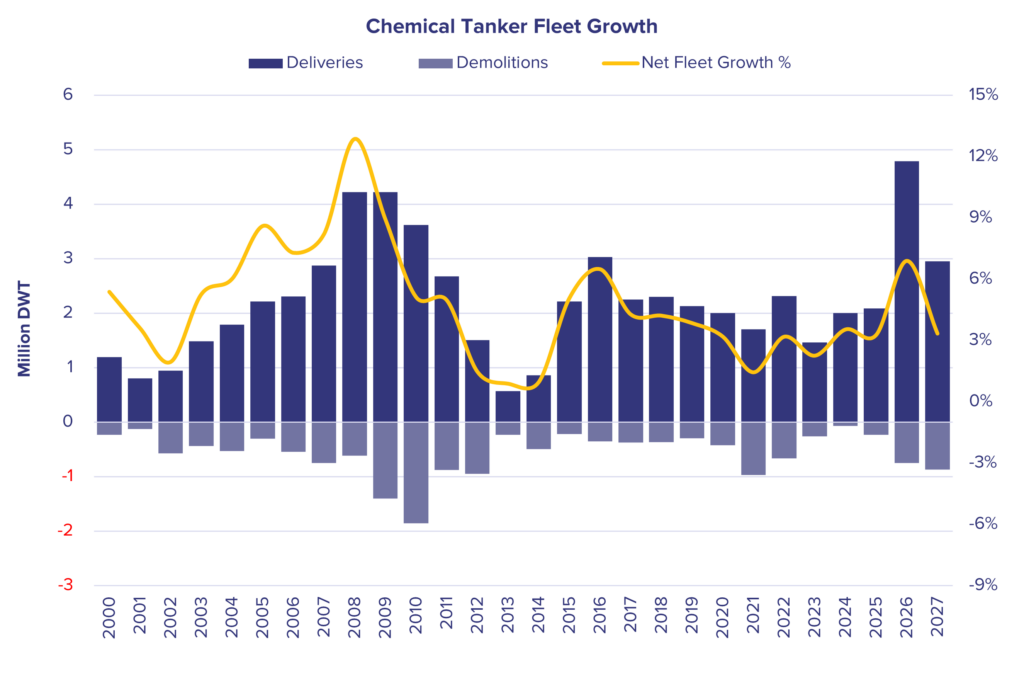

Following a wave of chemical tanker newbuilding expected through 2026, the orderbook will be thinning sharply, while new ordering activity remains subdued. Deliveries are expected to fall significantly from 2027 onward, while fleet removals at the same time are expected to be rising — particularly among less technically capable vessels as the fleet is aging. An increasing share of the global fleet is now over 20 years old, shrinking the pool of modern tonnage suitable for specialised cargoes.

“The headline fleet may look stable, but the effective supply of high-spec chemical tonnage is tightening every year,” says Preben Krohnstad, Director of Chemicals at IG’s Geneva office. “Modern coated and stainless-steel ships are increasingly hard to secure during peak demand periods, and that’s changing how charterers approach freight planning.”

Biofuels and ethanol reshape trade flows

One of the most significant structural shifts in chemical shipping has been the rapid growth of biofuels, biofuel feedstocks and ethanol.

Europe has emerged as a major import hub for these grades as decarbonisation policies and blending mandates accelerate. Long-haul flows from Southeast Asia, South America and the US Gulf have become structural, driving tonne-mile demand higher even when industrial chemical volumes soften.

Ethanol, in particular, has evolved from a largely regional product into a globally traded commodity. Global production now exceeds 110 million tonnes per year, led by the United States and Brazil, with increasing exports into Europe and Asia for fuel blending and industrial use.

Yet ethanol carries a very different risk profile from traditional clean petroleum products.

“Ethanol is far more technically demanding than many people realise,” explains Nicolau Mascarenhas, Director of Ethanol at IG. “Previous cargo history, coating condition and even minor tank residues can make a vessel unsuitable. The acceptable tonnage pool is much narrower than in mainstream product markets.”

As a result, ethanol is increasingly handled within the technical chemical tanker segment, intensifying competition for suitable vessels and elevating the importance of specialist broking expertise.

Global ethanol production now exceeds 110 million tonnes per year

Drawing on his background as a freight trader at Raízen, one of Brazil’s leading ethanol producers, Mascarenhas brings a trader’s perspective to freight optimisation. IG also provides freight-selling solutions, enabling clients to capture economies of scale.

“For example, if a client requires a 20,000-dwt lift, it can sometimes make sense to fix a 40,000-dwt vessel and market the excess space,” Mascarenhas explains. “That allows clients to reduce unit freight costs — and in some cases generate additional trading profit.”

The expanding role of the chemical shipbroker

With tightening tonnage supply and rising cargo complexity, brokers are playing a far more strategic role across technical assurance, market interpretation and risk management.

Technically, brokers now scrutinise coating compatibility, segregation options, heating capabilities, regulatory approvals and historical cargo records before presenting vessels to clients.

“One technical mistake can wipe out the economics of an entire trade,” Krohnstad says. “We’re no longer just fixing ships — we’re validating them.”

Freight volatility is also becoming more structural. Seasonal biofuel demand surges, regional congestion, longer trade routes and shifting tonnage positions are driving sharper rate swings than in previous cycles.

“Timing has become just as important as price,” Krohnstad adds. “Understanding when to lock in coverage, when to remain spot-exposed and how tonnage is repositioning between basins is where real commercial value is created.”

Risk management has similarly moved to the forefront. Chemical fixtures now sit within a complex framework of regulatory compliance, sanctions screening, environmental standards and heightened insurance scrutiny — particularly for biofuel and ethanol cargoes entering Europe.

“Execution quality matters more than ever,” Mascarenhas says. “Charterers are far less tolerant of operational surprises, delays or compliance issues. That puts a real premium on experience.”

He adds that some of the greatest value lies in technical creativity and optimisation.

“It’s about parcelling ships efficiently and identifying hidden capacity,” Mascarenhas explains. “An experienced broker might know that a 15,000-dwt restriction isn’t always absolute — perhaps an additional 300 tonnes can be safely loaded. That level of optimisation requires deep technical knowledge.”

Structural tightness — and macro factors — likely to persist

The outlook for chemical shipping remains supportive — but the industry is becoming increasingly specialised.

Trade volumes are expected to continue rising, supported by renewable energy transitions and specialty chemical demand. Biofuel and ethanol flows are becoming permanent components of global trade. Meanwhile, slowing fleet growth from next year onward and an ageing vessel profile are tightening effective supply.

At the same time, recent geopolitical developments — particularly in the Middle East — are adding a further layer of uncertainty to energy and chemical markets.

While no direct disruption to ethanol, biofuels or biofuel feedstock trades is expected, higher crude oil and gas prices are narrowing the pricing gap between traditional fuels and renewable alternatives. This dynamic is, in theory, supportive for biofuels demand and production.

Longer term, sustained energy market volatility could accelerate the strategic shift toward energy independence, reinforcing the role of biofuels within global energy systems. However, any immediate upside for shipping may be limited, given that major producing regions such as Brazil and Indonesia continue to prioritise domestic blending mandates.

“The broader direction is clear,” Krohnstad notes. “Biofuels are becoming a structural part of global energy supply, and those cargoes will continue to support demand for chemical tankers.”

Utilisation levels across key chemical trading regions are already firming, leaving less spare capacity to absorb demand surges.

“The market is becoming less forgiving,” Krohnstad adds. “There’s less spare capacity, more technical complexity and higher regulatory scrutiny. That combination naturally favours expertise.”

From intermediary to market partner

As the chemical tanker market evolves, success is increasingly defined by execution reliability and market insight rather than pure deal volume.

For charterers navigating complex ethanol trades, tightening tonnage pools and volatile freight cycles, brokers are becoming strategic partners rather than simple intermediaries.

“The role of the chemical shipbroker has fundamentally changed,” Krohnstad concludes. “Today it’s about understanding market structure, managing operational risk and helping clients make better decisions in a far more complex environment. Freight is no longer just a cost — it’s a competitive advantage when handled properly.”