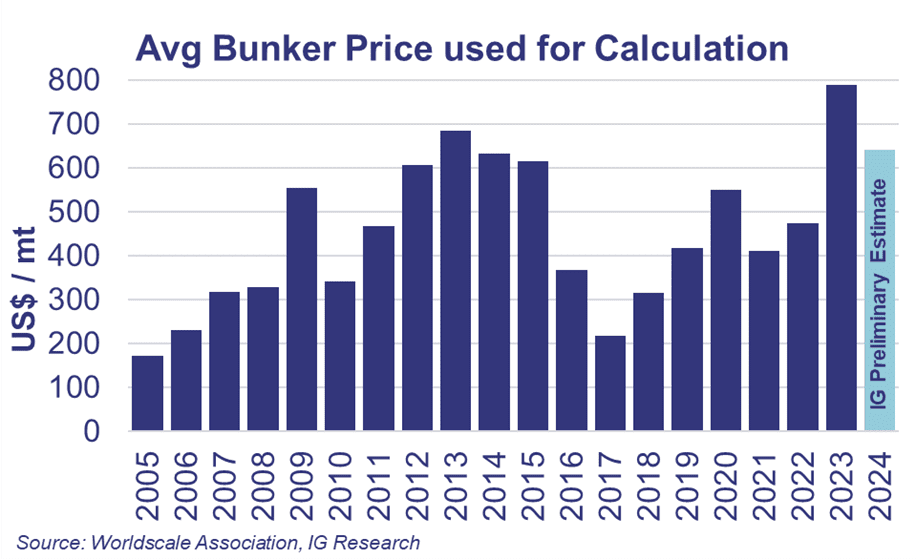

Changes in the voyage costs used for calculating the WS Flat Rates, between October previous year and end of September of the current year, will reflect on changes in next year’s Flat Rates. The changes in the voyage cost components are mainly focused around three areas, bunker costs, port costs and exchange rates with the focus remaining on the bunker price. Now that the WS Association have published their monthly (average) LSFO bunker prices, they can be utilised to get an understanding of potential changes in the Flat Rates for 2024.

After the strong growth of bunker prices over 2022, resulting in a 66% price rise over the October 2021 to September 2022, bunker prices continued their slow downwards journey from the heights of June 2022, almost reaching US$ 1,000 / mts basis LSFO. Then, from October 2022, bunker prices decreased further from US$ 733.39 / mt (accd to Worldscale), which marked the high point of the current calculation period. The lowest price points during were noted in May and June 2023 with monthly average prices just below US$ 580 / mt. However, with continued cuts by OPEC and non-OPEC countries of oil production, oil and by relation bunker prices, were stopped on their downwards journey and slowly worked their way back up to surpass US$ 670 / mt for the end of the observed timeframe. Considering that all necessary monthly bunker prices have now been published, we are not expecting any major changes in the bunker prices and would assume that the average bunker prices for the period prior to publication of the new WS rates are to remain mainly unchanged (chart 1).

Compared to the year prior, the annual average bunker price used for the 2024 Flat Rate changes show a reduction of around 20%. The last comparable period were the Flat Rate changes between 2020, when the bunker price changed from HSFO to LSFO and noted a decrease of around 25%.

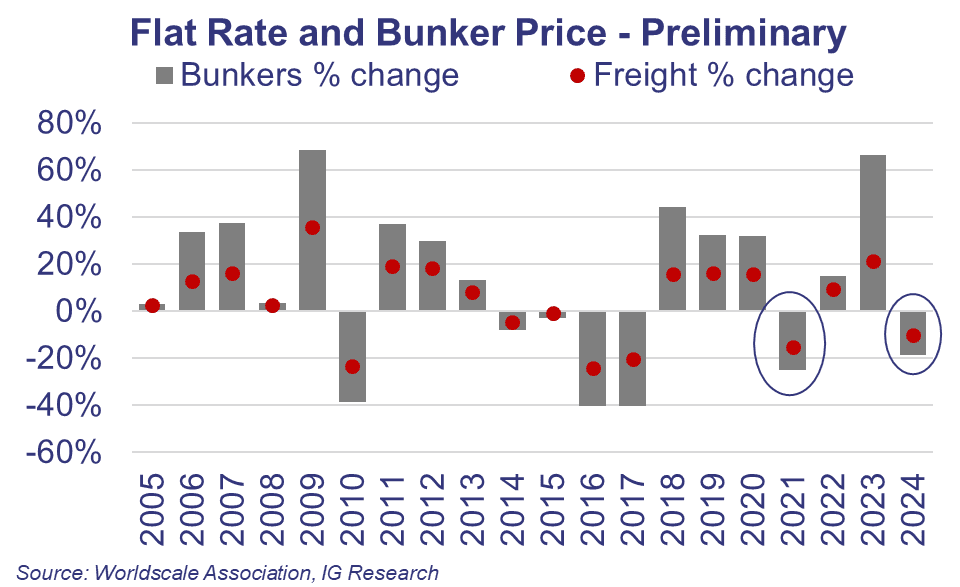

The question now is how the bunker price reduction will impact next year’s Flat Rates? As per our methodology, where we compare bunker price changes to actual changes in Flat Rates, IG Research estimates that average Flat Rates are expected to decrease by around 10%, again relatively close to the drop observed in the period between 2020 and 2021, as can be seen on the chart below (chart 2).

Of course, there will be some mild differences between long-haul and short-haul voyages. Naturally, long-haul voyage bunker cost represents a higher proportion of the overall voyage cost components, so the Flat Rate change is expected to be slightly larger. Equally, for the short-haul voyages, with bunker prices being a smaller proportion of the overall voyage costs, the change in Flat Rates is expected to be less significant, with short-haul Flat Rates dropping on average around 8% compared to 11% in long haul voyages.

Naturally, for the voyages completed entirely in an ECA zone, we have used slightly different methodology, as since 2016 rates schedule, prices of LSMGO of 0.1% sulphur content are used for the Flat Rates calculation for those voyages. However, as the representative MGO bunker costs grew and decreased in a similar percentage as the rest of the bunker prices, the Flat Rates that account for MGO are next year expected to decrease by around 8-9%, very similar to average non-ECA short haul voyage Flat Rates.