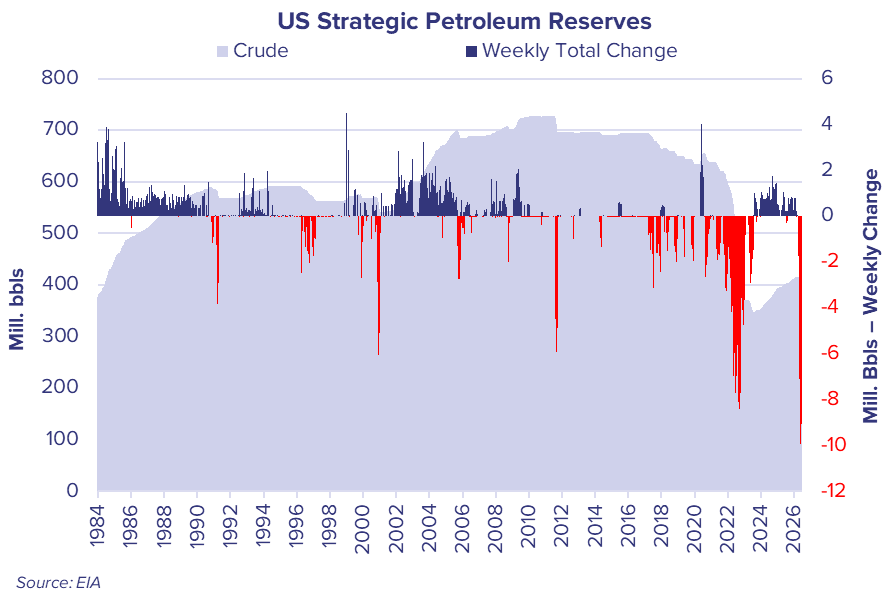

The US Strategic Petroleum Reserve (SPR) has been used relatively infrequently by the US administration since its inception in the 1970s. Aside from exchanges and operational movements, there have only been 4 emergency releases in response to significant disruption. The latest 172m bbl release, as part of a wider joint 400m bbl IEA release, marks the fifth such decision, and one of the largest on record.

Whilst part of the release will come in the form of exchanges (crude delivered today, with the obligation on the receiving company to restock the SPR at a later date), this release will likely see the SPR draw down to levels not seen since the inception of the reserve.

Releases have been accelerating in recent weeks, with the release for the week ending 22nd May seeing just over 9.9m b/d drawn, the equivalent of just over 1.4m b/d. This is the single largest weekly drawdown in SPR history.

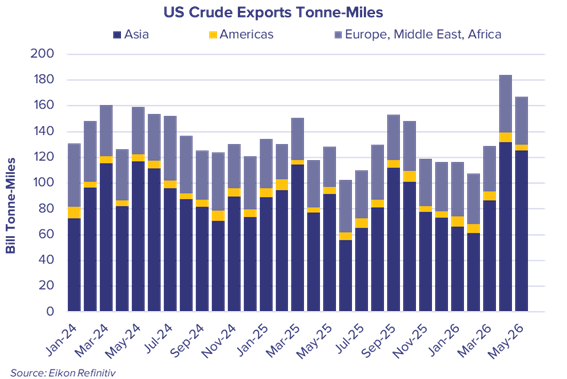

The SPR releases, coupled with the wider scramble for available cargoes has clearly supported increased US exports, which peaked at 6.4m b/d for the week ending 24th April, but broadly remain significantly elevated in recent weeks.

Volumes into Asian buyers have increased significantly across this period, with approximately 2.4m b/d of crude heading to Asia during April, a 1m b/d increase on the same month last year. May data suggests these levels have been sustained during the latest full month.

The impact on tonne-miles, especially for VLCCs have been significant, reaching recent highs and helping to provide some support to the segment in the face of demand destruction elsewhere.

Exports are likely to remain supported in the near-term by the SPR releases, however the current policy is scheduled to end around mid-July 2026. With the conflict in the Middle East seemingly at an impasse, and significant volumes of crude still taken out of the market, this end date approaches quickly, and the question as to what happens next becomes more relevant…