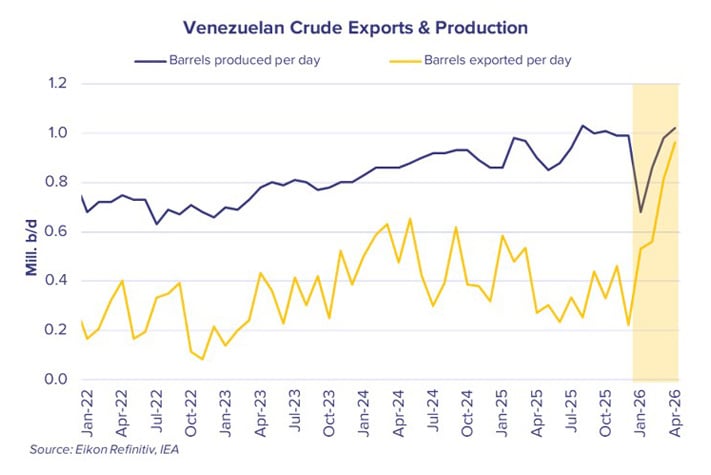

In January, acting president of Venezuela Delcy Rodríguez announced a target of 1.37m b/d of crude production by the end of the year. Should this be achieved, it would again reach levels last seen in 2018 and mark a significant uptick on the low point of 360,000 b/d seen in 2020.

Venezuelan crude exports have been under a variety of pressures in recent years; most notably, sanctions and logistical constraints on lifting barrels from the under-maintained and under-invested infrastructure have capped volumes well below reported production levels.

However, the past few months in the post-Maduro regime have seen a dramatic push on export volumes, with the spread between production and exports narrowing significantly. Reported April crude exports sit at just over 960,000b/d, the highest monthly total seen since 2019.

Oil major activity and interest in Venezuela continues to grow, with reports suggesting that Chevron, BP, ENI & Repsol have all increased their exposure in the country. The Venezuelan government is expected announce new legislation providing clarity to investors. The new framework is anticipated to include international arbitration, allowing for disputes to be resolved outside of Caracas, potentially easing investor concerns and smoothing the path towards the rejuvenation of Venezuela’s oil industry.

Venezuelan crude shifts away from China – higher volumes heading to US, Europe and India

The United states has increased imports of Venezuelan crude since the removal of Maduro on the 3rd of January, with consecutive monthly increases in Venezuelan flows to the US, resulting in over 380,000 b/d discharging in the US in April, the highest figure since December 2018. With US Gulf refineries predominantly set up to process heavy crude, demand for Venezuelan blends is likely to persist. The US satisfied its heavy crude demand with Canadian oil after sanctions were placed on Venezuela. With the US playing a heavy role in Venezuela’s oil industry in the immediate future, its demand for Venezuelan crude could likely tend toward pre-sanction levels.

2026 has seen the Americas take the majority of exported Venezuelan crude, however not all of this is going to the US. 2026 has exhibited some of the highest levels of Venezuelan crude discharging in the Caribbean since 2018, with just over 215,000 b/d in April. These are likely not end destinations for the crude but acts as Ship-to-Ship transfer and storage locations, obscuring the destination of the crude.

The relaxation of sanctions, and the events in the Middle East have seen Venezuelan barrels head to more varied destinations. There has been a significant increase in crude exports to India, with March exports reaching their highest level since 2020. In April, Spain imported just above 90,000 Bpd of Venezuelan crude, around 10% of exports that month.

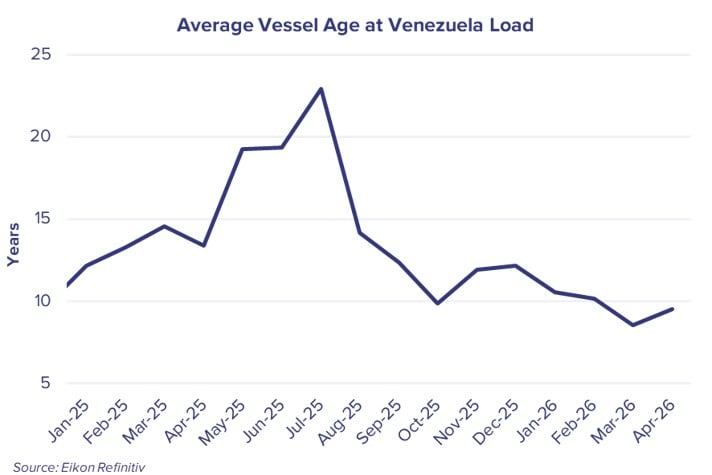

VLCCs are the dominant size for venezuelan exports

As the chart shows, the average age of the vessels loading in Venezuela dropped significantly through the second half of 2025 and continued on a downward trend since. The reduction in age profile indicates a significant shift towards more market-based tonnage, away from ‘premium-focussed’ grey fleet vessels, especially as volumes shifted away from China to alternate buyers.

Data indicates that, in 2026, VLCCs have lifted a significant share of Venezuelan crude exports, a substantial amount of these characterised by the increase of flows to India.

The combination of growing exports and a pivot towards market tonnage, should offer positive tonne-mile upside to crude tankers, especially VLCCs, operating within the Atlantic basin.

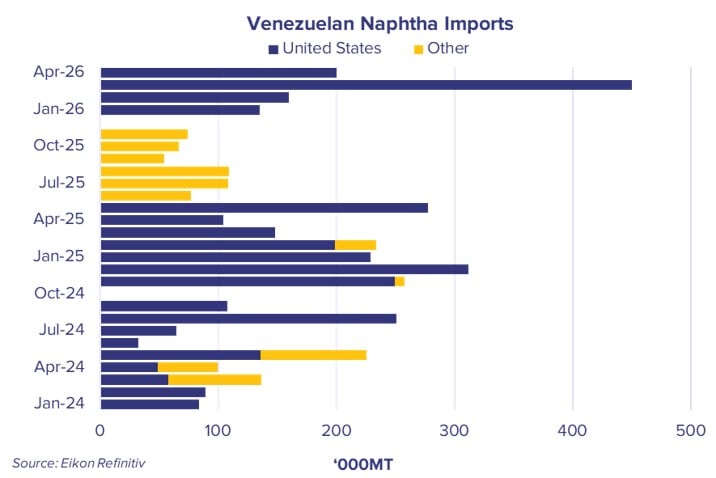

Will a tight naphtha market cause problems for Venezuelan crude exports?

Naphtha is vital to Venezuela in order to dilute the various heavy crude grades and make them suitable for export.

The data illustrates how in recent months, following the removal of Maduro, the US has effectively monopolised Venezuelan naphtha imports, replacing the previously dominant Russian volumes. March 2026 exhibited the highest amount of naphtha entering Venezuela since our data began in October 2018, with over 450,000mt of naphtha being imported, the equivalent to 40% of the US total monthly naphtha exports. All of this was lifted by LR1s, signalling a potential growing trade for the LR1 market.

The Venezuelan naphtha trade does not operate in a vacuum. In their latest report, the IEA illustrates the declining Asian demand for naphtha in response to the supply shock of the Middle East conflict. Middle East naphtha exports have dropped from around 135,000 mt/day in 2025 to around 29,000 mt/day in April 2026. Traditional buyers of Middle Eastern naphtha initially cut feedstock imports, however as the conflict continues, some buyers are looking elsewhere for cargoes. Notably, South Korea and Japan took a combined 485,000 mt of US naphtha during April, with both countries having strong histories of importing naphtha from the United States.

As the disruption continues, Venezuela may have to compete with Asia for naphtha cargoes, potentially placing a constraint on crude exports.

For further insights, contact [email protected].