The ban can be looked at through the prism of disrupted fertiliser and sulphur trade flows and the government’s increased focus on providing price and supply stability for the domestic sulphuric acid and fertiliser markets.

The ongoing trade disruptions in relation to the Iran war effectively stopped the fertilisers exports from the region. Furthermore, sulphur which is used for sulphuric acid production, which is in turn used for phosphate fertiliser production is another commodity export flow that is heavily affected. China is one of the countries that is very dependable on MEG sulphur exports. Prior to the conflict the region supplied 38% of all sulphur imports into China.

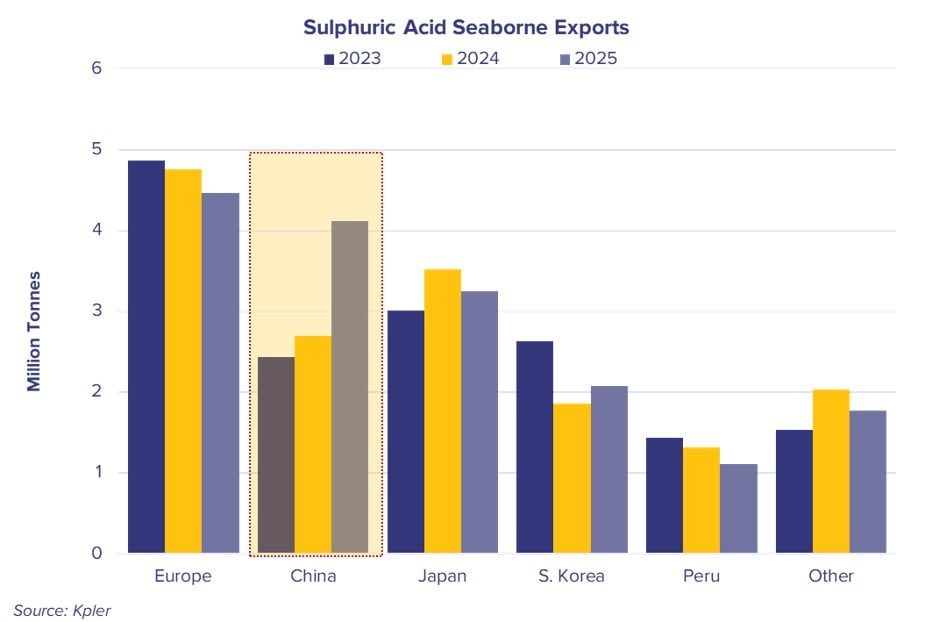

Over the last few years China became the largest sulphuric acid exporter, and the ban is expected to influence the chemical tanker market sector, especially stainless steel tankers.

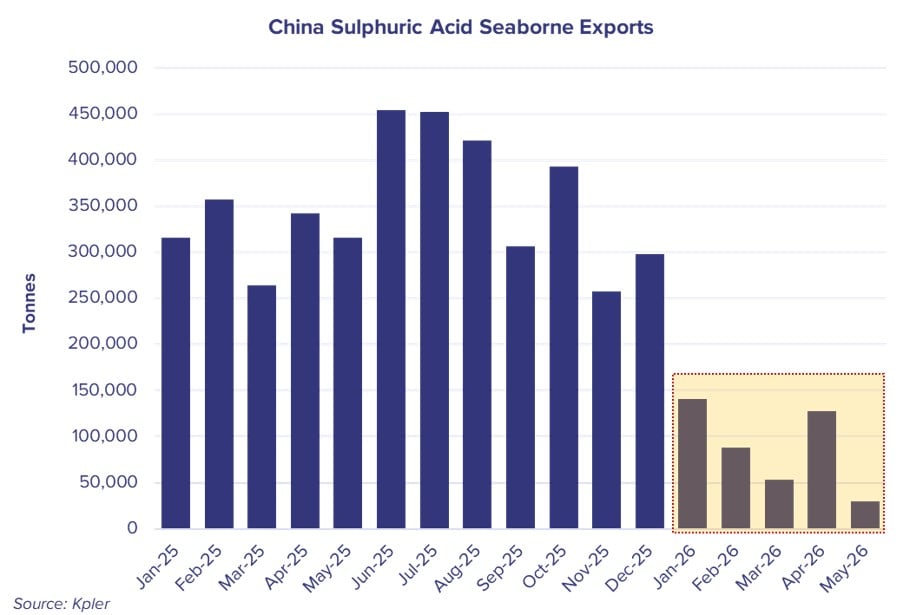

Even prior to the recently announced sulphuric acid exports ban, Chinese exports were curtailed by the reported export quotas during 2026. Year on year for the period between January and April, the export volumes dropped by more than 2/3rd between 2025 and 2026. This helped to ‘shield’ domestic sulphuric acid prices from the strong rises recorded in the last few months globally.

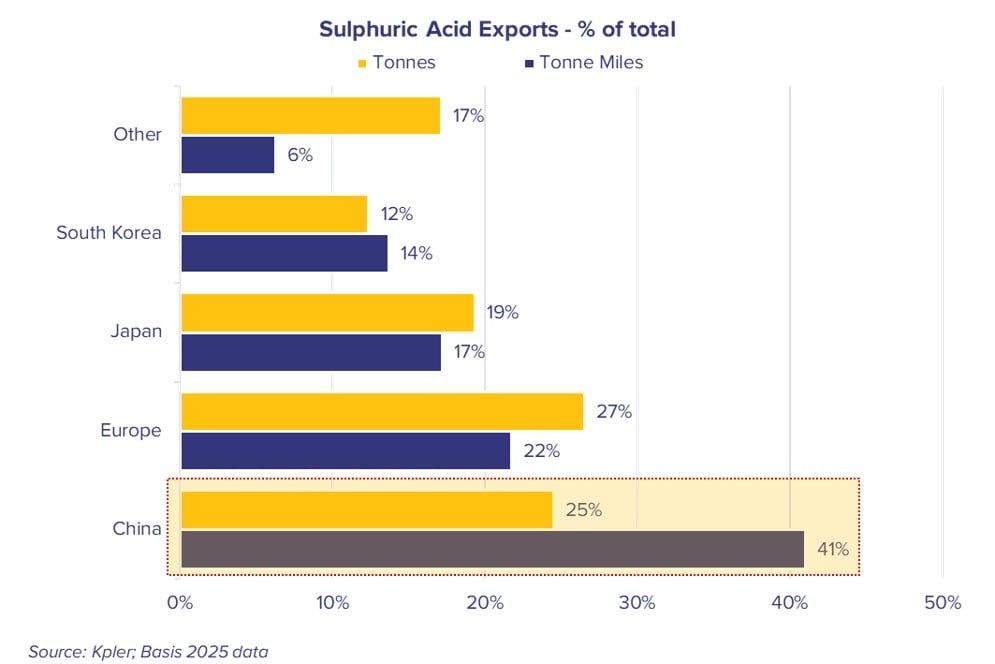

Despite exporting 1/4th of the global seaborne volumes, the Chinese sulphuric acid exports contributed around 41% of the global sulphuric acid tonne miles in 2025. Overall Chinese sulphuric acid exports contribute 20% to the stainless steel tankers utilisation. Majority of the Chinese exports are aimed at Chile for metal production and India and Morocco for fertiliser production.

Chinese sulphuric acid exports are still a very small percentage of the overall domestic production and production capacity. Similarly to the recent CPP export bans, the policy may be subject to revision down the line. However, this is still a subject to the geopolitical developments and in connection with already disrupted MEG sulphur exports.