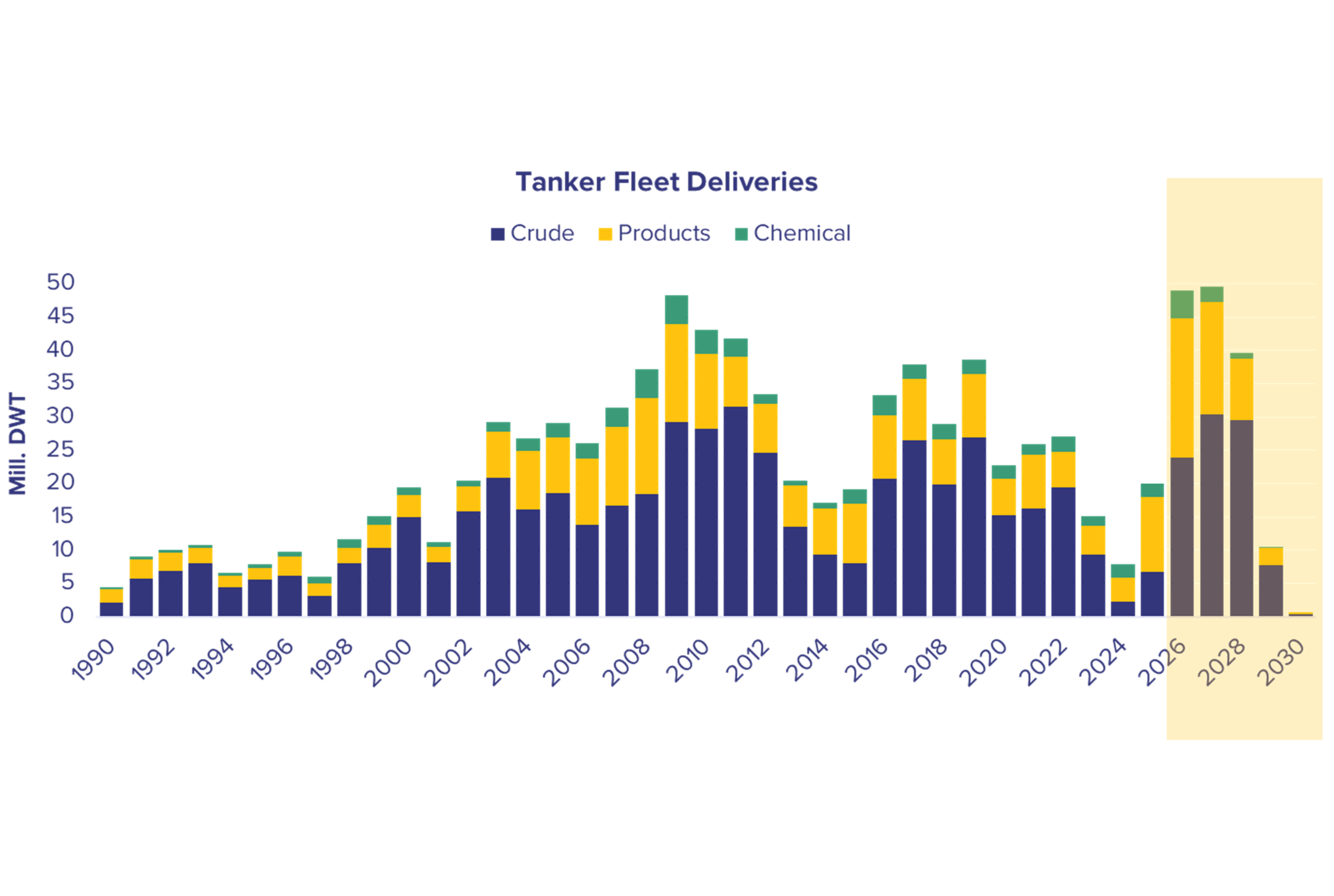

After a couple of years of relatively modest tanker fleet growth, last year we entered a period of more fleet additions. Although it is worth noting that in relative terms the total tanker fleet capacity growth was not spectacular, as the capacity delivered remained below yearly average for the 2015-24 period.

This year alone 49 million dwt of tanker fleet capacity is scheduled to be delivered. If no significant slippage is recorded, 2026 looks set to top 2009’s 48 million dwt delivery tally. Notably, a significant number of vessels have already hit the water this January, as some vessels originally slated for delivery for the end of last year were pushed into 2026. Next year’s deliveries are expected to remain high, edging closer to 50 million dwt according to the current delivery schedule.

More crude oil tankers

As we noted in our November report, the product tankers dominated tanker fleet deliveries last year, accounting for close to 57% of the total delivered capacity. Crude oil tankers and chemical tankers deliveries were 33% and 10% of total capacity respectively. However, from this year onwards, this ratio is going to shift towards the crude oil tankers fleet. This year close to half (49%) of the total capacity delivered in dwt is expected to be in the crude oil tankers segment, while product tankers should account for 42% and chemical tankers anticipated to amount to 9%.

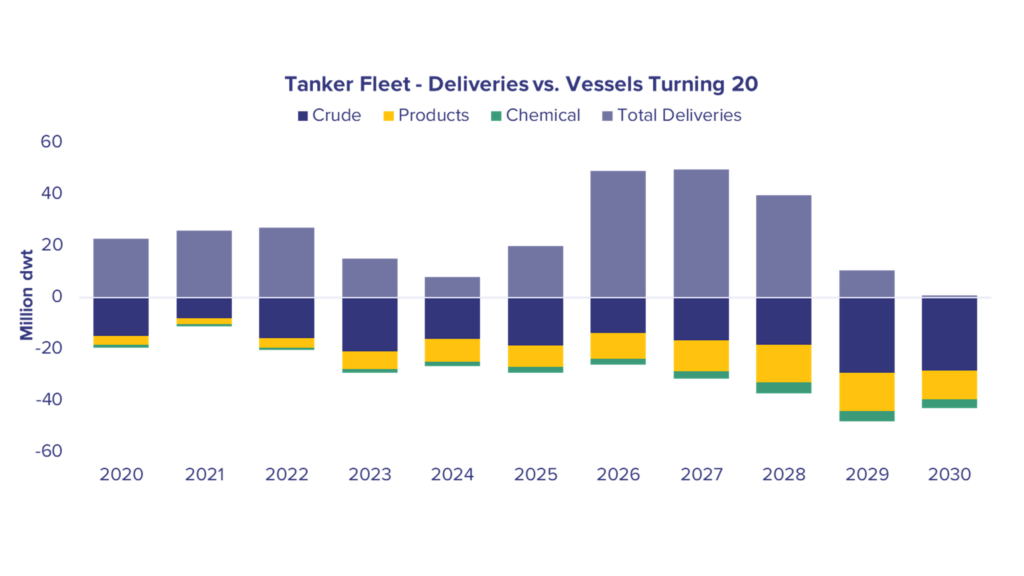

Driven by the recent surge in newbuilding orders — particularly for larger crude oil tanker segments such as VLCCs and Suezmaxes — the crude tanker fleet is set to dominate the delivery schedule going forward. Its share of total delivered capacity is projected to rise to nearly two-thirds in 2027 and 75% in 2028, based on the current orderbook. All in all, the crude oil tanker segment is expected to see close to 24 million dwt delivered this year with around 30 million dwt expected to be delivered in 2027 and in 2028. Even so, the expected cumulative 2026-2028 delivery schedule is still below the 89 million dwt of crude oil tanker delivered between 2009-2011. With the fleet expected to significantly age towards the end of the decade, much of this incoming capacity is likely to replace older ageing tonnage rather than flood the market.

Product tanker deliveries hit highs

Product tanker fleet deliveries are expected to reach a historic peak, as around 20 million dwt of capacity is expected to hit the waves. Growth is going to be driven by all three major segments, with MR and LR2 deliveries leading the way.

However, recently “rediscovered” interest in LR1 tonnage means that this segment is building momentum. 70 ships are currently on order and scheduled for delivery by 2029.

As last year’s interest firmly switched to larger crude oil tankers, the product tankers fleet deliveries are expected to tail off from next year onwards. However, next year’s deliveries are expected to remain elevated as roughly 17 million dwt of newbuilding capacity is expected to be delivered in 2027.

Chemical tankers near peak

The chemical tanker fleet is also expected to surge, peaking this year as close to 4.3 million dwt is expected to be delivered. These are similar levels as the delivered capacity recorded in 2008 and 2009. But this momentum is unlikely to last. Newbuilding orders slowed significantly down during 2025, as less than a quarter of the orderbook capacity placed in a year prior was booked in the yards.

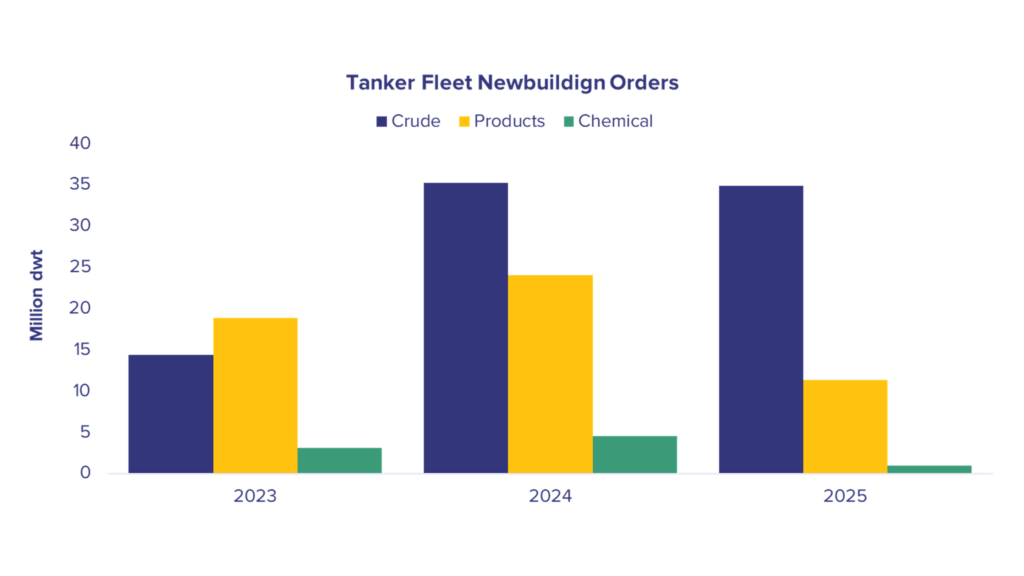

Uncertainty impacted 2025 orders

A large crude oil tankers fleet accelerated newbuilding activity in Q4 last year spurred by stronger earnings, particularly in the VLCC segment. On the other hand, most other tanker segments saw a significant drop in the newbuilding capacity ordered compared to 2024.

Geopolitical turbulence between some major trading partners weighed directly and indirectly on newbuilding orders. The outlook beyond 2028 points to more modest fleet growth. Crucially, this coincides with a rapidly ageing global tanker fleet — a dynamic that should help absorb much of the capacity currently on order. Demand for younger, more fuel-efficient vessels is likely to remain strong.